Countdown to Coverage Collapse

As ACA subsidies expire, the GOP offers no replacement — just rhetoric, risk, and rising costs.

When Donald Trump first ran for president in 2016, he promised that his administration would deliver a health care plan that was better, cheaper, and covered everyone. For four years, he insisted that a comprehensive plan was just “two weeks away.” That moment never arrived. His administration attempted to repeal the Affordable Care Act in 2017 and failed. The promised replacement never materialized. Instead, what followed was a patchwork of executive orders, deregulation efforts, and messaging designed to undercut the ACA without offering a real alternative.

Now, in his second term as president, having returned to office on January 20, 2025, Trump is making the same promises all over again. He continues to attack the ACA, calling it broken, expensive, and outdated. Yet once again, there is no actual plan on the table. No bill. No policy blueprint. No numbers that demonstrate how his approach would improve coverage or lower costs. The closest thing to a “plan” so far is a loosely defined strategy that includes cutting subsidies, expanding Health Savings Accounts, deregulating private insurance, and reducing federal involvement. It’s less a health care policy than a tax shelter scheme dressed up in populist rhetoric.

Most importantly, not a single element of this so-called plan would increase access, reduce costs, or improve care for ordinary Americans. There is nothing here that meets the moment, especially not with a major deadline looming.

Want to Know Your Rights?

Download a free digital copy of the U.S. Constitution—the same document Trump is trying to bulldoze. Learn exactly what he’s breaking… and how to fight back.

75,000+ strong — and counting.

This Black Friday & Cyber Monday, become a paid subscriber for just $1 a week and help us keep the truth alive.

Join The Coffman Chronicle — $1/Week Early Access

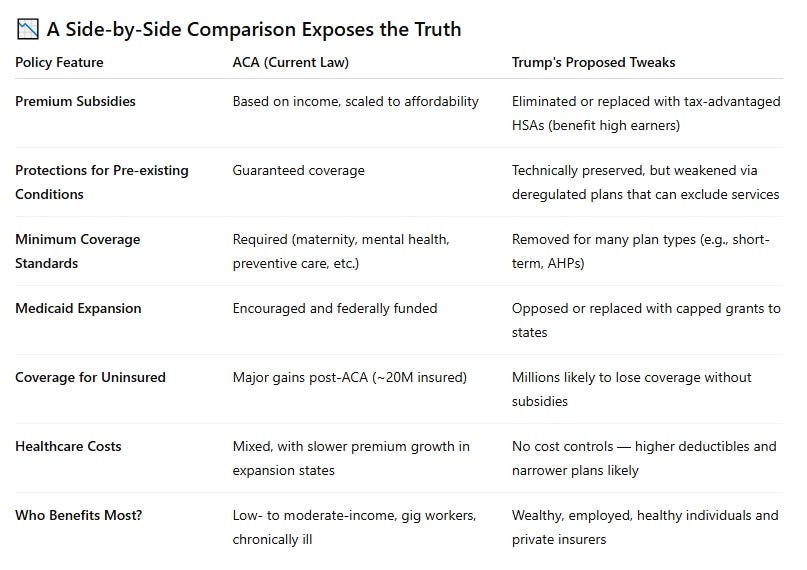

What the GOP Is Actually Proposing

Despite controlling the White House and exerting strong influence in Congress for nearly a year, Republicans have not presented a comprehensive health care policy to replace or reform the Affordable Care Act. What they have offered, instead, is a series of loosely connected ideas that amount to little more than a rollback of the ACA’s core protections.

At the center of the current GOP posture is the looming expiration of enhanced ACA subsidies, which were extended under the Biden administration through 2025. These subsidies have helped millions of Americans — especially low- and middle-income individuals who don’t get insurance through an employer — afford health coverage through the ACA marketplace. The deadline for renewal is December 31, 2025. If no action is taken, premiums will rise sharply in 2026, and coverage losses will follow. The Trump administration has signaled it does not support a clean extension.

Instead, the White House and congressional Republicans have floated the idea of transitioning away from direct subsidies and toward tax-advantaged Health Savings Accounts (HSAs) and employer-centered Health Reimbursement Arrangements (HRAs). These tools benefit individuals who already have disposable income or are securely employed, but they do little for low-income or part-time workers, those with chronic conditions, or people in rural or gig-based jobs.

Meanwhile, other Republican leaders are reviving old ideas, including lifting regulations on insurance providers, allowing more short-term or association health plans that don’t have to meet ACA coverage standards, and shifting Medicaid funding to capped grants, all of which reduce federal responsibility and weaken consumer protections.

What’s not included in any of these proposals is a serious plan to reduce the actual cost of care, whether it’s hospital visits, prescription drugs, or preventative treatment. Nor is there any mechanism for expanding access to the uninsured. The rhetoric is about “freedom” and “flexibility,” but the policies are simply about spending less, not achieving more.

Who Loses Under These ‘Tweaks’

For all the talk of reform and innovation, the reality of the GOP’s health care posture is simple: it shifts costs and risks downward, away from the government, away from insurers, and directly onto the backs of ordinary Americans.

If enhanced ACA subsidies expire at the end of 2025 with no replacement, the impact will be immediate. Millions of Americans will wake up in January 2026 facing monthly premiums that are two or even three times what they paid the year before. For some, particularly those whose incomes place them just above the Medicaid threshold but far below the comfort of employer coverage, insurance will become unaffordable overnight.

The Urban Institute estimates that up to 4.8 million people would lose their coverage in 2026 under this scenario. That’s not a marginal effect. It’s a public health rollback. For many, it will mean going without preventive care, delaying treatment, or facing bankruptcy if a major illness strikes.

These policy shifts hit specific groups hardest, including low-income workers without employer insurance, self-employed and gig workers who rely on ACA plans to access care, older adults in the pre-Medicare years, rural Americans with few coverage options, and anyone with a chronic condition who can’t afford to gamble on a low-cost, high-deductible plan. Essentially, it harms everyone the ACA was designed to serve.

And for those who do try to maintain coverage, the financial strain grows heavier. Under current estimates, a single person making around $28,000 a year could see their premium jump from a few hundred dollars annually to over $1,500, a fivefold increase. That’s not a gentle phase-out. That’s a policy cliff.

These aren’t just numbers. These are people’s lives, health, and financial stability. Under the GOP’s approach, they’re being treated as collateral damage.

Who Wins

While the human cost of these policy shifts is staggering, the political and economic beneficiaries are much easier to identify. Predictably, if the Republican “tweaks” to the health care system take effect, insurance companies and high-income earners stand to gain the most.

By promoting Health Savings Accounts and employer-based reimbursement arrangements as alternatives to direct subsidies, the GOP is steering benefits toward those who already have resources. HSAs are most advantageous to people with higher incomes, because they allow untaxed savings to be set aside for medical expenses, a useful tool if you have money to spare. However, for lower-income individuals living paycheck to paycheck, the idea of “saving” for future care is unrealistic. There’s no tax break if you have no money to save.

At the same time, deregulation efforts that would expand short-term and association health plans — options that don’t have to meet ACA standards — open the door for insurers to offer lower-premium products that cover less. These plans may be attractive to healthy individuals in the short term, but they pose real risks to anyone who later develops a serious medical condition. For insurers, they’re a windfall. There are fewer requirements, lower payouts, and steady premiums.

Employer-sponsored plans also come out ahead under the Republican framework, especially large companies that can shift more responsibility to workers through tax-friendly reimbursement models. However, if you’re unemployed, self-employed, or working part-time, there’s nothing here for you.

The common thread across these changes is that the people and industries with power and financial security are being given more options and more advantages. Everyone else, especially those who have come to rely on the ACA for stability, is left with fewer protections and higher costs.

This isn’t an oversight. It’s the design.

The Ticking Clock

The consequences of this policy drift aren’t theoretical. They’re on the calendar. On December 31, 2025, the enhanced subsidies under the Affordable Care Act are set to expire. These subsidies have made health insurance affordable for millions of Americans who otherwise would have been priced out of coverage. If they are not renewed or replaced with an equally robust alternative, the fallout will begin immediately in 2026.

And here’s the political reality. There is no plan in place.

The Trump administration has made clear that it opposes a clean extension of the subsidies. Republicans in Congress are divided, with some echoing the president’s preference for redirecting support into health savings accounts, while others remain silent. No consensus exists. No legislation has been introduced, and the clock is ticking.

The result is a looming policy cliff just months before the 2026 midterm elections. Americans will begin receiving notices about their 2026 health insurance premiums in late fall. Those who shop for plans during open enrollment will discover that many of the low-cost options they relied on have vanished. Some will see their premiums double. Others will be forced to drop coverage entirely.

This isn’t just bad policy. It’s a political time bomb. When voters head to the polls in November 2026, many will have just faced the harshest health insurance market in years, and they’ll know exactly who let it happen.

The GOP’s Strategy: Avoid Comparison

In any honest policy debate, the question should be simple: which plan helps more people, at a lower cost, with better outcomes? If the Republican alternative to the ACA were truly superior, we’d have seen a side-by-side comparison long ago, a bill, a framework, even a set of projected numbers showing how many people would gain coverage, how much they’d save, and how health outcomes would improve.

But that’s not what we’re getting.

Instead, we’re watching a familiar pattern. Republicans criticize the ACA for its perceived costs or imperfections yet offer no comprehensive replacement. The proposals being floated — HSAs, deregulated plans, state waivers — are abstract tools that favor those already doing well. They don’t add coverage. They don’t lower costs. They don’t expand access, and they certainly don’t confront the structural forces driving American health care inflation.

So rather than debate the ACA on equal footing, the GOP is relying on rhetoric. Words like “freedom,” “choice,” and “innovation” are used to mask the reality: their policy vision shifts financial and medical risk onto consumers while removing guardrails for insurers. It’s a sleight of hand. They’re not fixing the system. They’re stepping back from it.

The refusal to present a real, measurable alternative speaks volumes. It’s not because the math is hard. It’s because the truth is harder. When put side by side, the ACA remains the stronger policy for those who need health care most. And that’s a comparison the GOP is unwilling to have, because it’s one they know they’ll lose.

We Deserve Better

The Affordable Care Act was never perfect. It was a compromise from the start, a market-based solution to a deep structural crisis. However, it expanded access to millions, established real protections for people with pre-existing conditions, and brought a measure of stability to families who had long lived at the mercy of insurance companies. It didn’t fix the system, but it made it better.

What we’re seeing now is not an effort to improve on that progress. It’s an effort to undo it. The Republican strategy, from President Trump on down, is to let the ACA falter by design, to let subsidies expire, to let people be priced out of care, and to do all of it without offering a serious alternative in return.

This is not leadership. It’s abdication.

Health care is not a theoretical debate. It’s a monthly premium, a prescription refill, a doctor’s visit when your child has a fever. It’s the difference between catching a disease early or too late, between manageable debt and medical bankruptcy, between life and death.

We deserve a policy debate grounded in reality, not slogans. We deserve lawmakers who will tell us the truth, who will present real plans, with real numbers, and stand by them. We deserve a system that covers more people, costs less, and delivers better care.

We don’t have to settle for less. We certainly shouldn’t settle for nothing.

Don’t let the bastards sneak anything past you. Subscribe and get your daily dose of rage and receipts delivered fresh, before the spin doctors can scrub it.

Sources:

“4.8 Million People Will Lose Coverage in 2026 If Enhanced Premium Tax Credits Expire” — Urban Institute, September 17, 2025

“Providers face $32.1B in lost 2026 revenue if ACA subsidies expire” — Fierce Healthcare, September 26, 2025

“Trump weighs plan to extend extra ACA subsidies for two years” — STAT, November 24, 2025

“Health‑care proposal floated by White House runs into familiar GOP divisions” — PBS, November 26, 2025

“Changes in Health Care Spending and Uncompensated Care Under Enhanced Tax Credit Expiration” — Urban Institute, September 25, 2025

“Clash over healthcare subsidies threatens to reshape 2026 midterms” — Reuters, November 14, 2025

“Trump says he would prefer not to extend Obamacare subsidies” — Reuters, November 25, 2025

“GOP faces a familiar dilemma: What to do about Obamacare?” — The Washington Post, December 1, 2025

“Senate barrels toward failure on health care” — Politico, December 1, 2025

“Some Americans fear high health‑insurance premiums if ACA enhanced subsidies expire: ‘Very much a worry’” — ABC News, October 21, 2025

Read Clara Mattei's book: The Capital Order: How Economists Invented Austerity and Paved the Way to Fascism.

When the people are weakened they are easily subjugated.

If Obama had not proposed ObamaCare, Republicans would have proposed it. It preserves the current system of private medical care paid by private insurers. A provides a subsidy to low income participants in the insurance market and requires a level of coverage, but otherwise the government is not involved.

I once joked to some folks with the California health insurance regulator that they should offer a low cost plan that only uses therapies that are no longer under patent protection. They laughed and said they considered a plan called yesterday’s care at yesterday’s prices, but concluded it would not get support.