Defining the Limits

The Department of Justice can define the scope of a settlement. Can it define the limits of governmental authority?

In the span of just twenty-four hours, two reports raised questions about potential conflicts of interest involving President Donald Trump and those close to him. One examined reported connections between businesses associated with the Trump and Lutnick families and federal mining initiatives. The other questioned the timing of the president’s reported investment in Axon Enterprise relative to a major Immigration and Customs Enforcement procurement effort.

Whether either report ultimately withstands scrutiny remains to be seen, but the reports raise a more immediate institutional question. If credible evidence of wrongdoing involving a public official were to emerge tomorrow, what authority would the federal government have to investigate it?

A Department of Justice memorandum issued on May 19 has prompted competing interpretations among legal observers, members of Congress, and former Justice Department officials. Courts may ultimately define the memorandum’s scope, or they may never be asked to do so. The constitutional questions raised by the document exist regardless.

The issue is not simply what the memorandum means, but more importantly, what it suggests about how the government understands the limits of its own authority.

If you value analysis that looks beyond today’s headlines, consider subscribing.

We examine how current events reshape the balance of power among the branches of government, the role of independent institutions, and the precedents today’s decisions leave for future administrations. Our goal is not to tell you what to think, but to ask the constitutional questions that often go unexplored in the daily news cycle.

Join a community committed to understanding not just what happened, but what today’s decisions mean for the republic we leave tomorrow.

The Memo

The memorandum at the center of this discussion originated from a lawsuit arising from the leak of confidential taxpayer information by former Internal Revenue Service contractor Charles Littlejohn. Littlejohn later pleaded guilty and was sentenced in federal court. According to the IRS, more than 400,000 taxpayers were ultimately notified that their information may have been affected by the breach.

President Donald Trump, Donald Trump Jr., Eric Trump, and the Trump Organization subsequently sued the federal government, alleging that the IRS and the Treasury Department failed to adequately safeguard their confidential tax information.

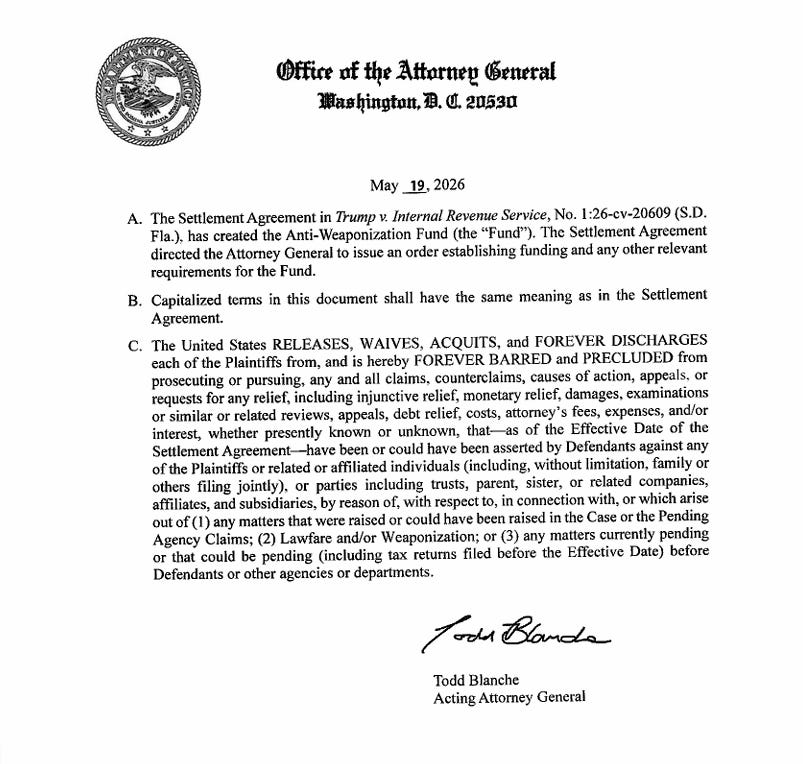

A settlement was announced in May. On May 19th, Acting Attorney General Todd Blanche released an agreement establishing a proposed Anti-Weaponization Fund and directing the Attorney General to take the necessary steps to implement it. Ten days later, however, a federal court paused the fund while legal challenges moved forward. Although the administration has since stated that the fund is no longer moving forward, litigation surrounding that portion of the settlement has continued.

Far less attention has been paid to other provisions of the agreement. The memorandum does more than establish the Anti-Weaponization Fund. It also contains a release provision stating that the United States “RELEASES, WAIVES, ACQUITS, and FOREVER DISCHARGES” the plaintiffs and is “FOREVER BARRED and PRECLUDED” from pursuing action. Those categories include highly specific references to tax returns filed before the agreement’s effective date, as well as broader language referring to claims that “have been or could have been asserted,” matters “currently pending or that could be pending,” and actions involving other agencies or departments.

Almost immediately, the memo produced sharply different interpretations. Some legal observers viewed it as a narrow provision intended to resolve the tax leak dispute. Others pointed to broader language, arguing that the memorandum’s scope was less clear than its defenders suggested.

During subsequent congressional testimony, Blanche argued that the memo should not be understood as granting blanket immunity from future investigations.

Precision Is Not a Technicality

Legal drafting is often viewed as a technical exercise. At the Department of Justice, it is considerably more than that. The nation’s chief law enforcement agency does not simply interpret the law. Its memoranda communicate how the Executive Branch understands the authority entrusted to it by Congress and, ultimately, by the Constitution. Those documents become part of the public record. They are read not only by the parties before the Department, but also by federal agencies, members of Congress, courts, and future administrations. Precision is not merely a matter of style. It is an institutional obligation.

The May 19 memo demonstrates that the Department knew how to draft with specificity when it chose to do so. It refers to tax returns filed before the agreement’s effective date, clearly identifying both the subject matter and the relevant period.

Elsewhere, however, the memo uses broader language. It refers to claims that “have been or could have been asserted,” matters “currently pending or that could be pending,” and actions involving “other agencies or departments.” Despite Blanche’s assurances to Congress, the language in the memo persists. It has not been amended or reissued.

People can disagree about the correct interpretation of a legal document. That is not remarkable. What is remarkable is when that disagreement concerns a memo issued by the Department of Justice defining the scope of governmental authority. In that context, precision serves a constitutional purpose. Clear language promotes public confidence that governmental power is being exercised within identifiable boundaries rather than leaving those boundaries to later explanation.

We should not have to rely on future testimony or litigation to understand what an official Department of Justice memorandum does. It should be drafted cleanly.

Whose Authority?

Questions about the memo do not end with its word choice. They are also concerned with the implied authority reflected in the commitments it makes.

The litigation arose from the leak of confidential taxpayer information by a former IRS contractor, yet the memo’s release language does not refer only to the IRS. It also references “other agencies or departments,” expanding the discussion beyond the agency whose actions gave rise to the lawsuit.

The public record does not clearly establish whether the memo merely makes official conclusions already reached by the IRS, reflects commitments made solely by the DOJ in settling the litigation, or represents a broader understanding of obligations that extend across executive agencies. Those possibilities carry different constitutional implications. Under what authority does the DOJ speak for all executive agencies?

The same observation applies to the parties covered by the memo. The lawsuit itself identifies specific plaintiffs. The release language, however, extends beyond those named parties to include broader categories such as related or affiliated individuals, “family or others filing jointly,” trusts, parent or related companies, affiliates, and subsidiaries. While legal releases may define covered parties more broadly than the plaintiffs, every additional category is presumed to serve a purpose. It is reasonable to ask what work the broader language was intended to perform.

The memorandum also combines highly specific language concerning tax returns filed before a defined date with broader provisions addressing claims that “have been or could have been asserted” and matters “currently pending or that could be pending.” Under what authority can the DOJ determine that the settlement of this specific case warrants such expansive decisions?

The Need for Limiting Principles

Constitutional government depends upon more than the existence of authority. It depends upon the existence of limits.

Every branch of government exercises discretion. Prosecutors decide which cases to pursue. Regulatory agencies determine how best to enforce the laws Congress has enacted. Courts decide how legal principles apply to individual disputes.

Discretion, however, is not the same as unlimited authority.

The constitutional question raised by the Blanche memo is not whether the DOJ possessed the authority to settle a lawsuit. The more consequential question is where that authority ends, and how far they can or did attempt to stretch it.

If the memo is to resolve the claims from the Littlejohn litigation, the limiting principle is relatively straightforward. The settlement resolves a defined dispute involving identified parties and identified claims. If, however, the memo extends beyond those confines, the limiting principle becomes less apparent, raising serious questions.

What happens if substantial new evidence emerges? What if another executive agency, acting under authority delegated to it by Congress, concludes that additional inquiry is warranted? What if circumstances arise that no one anticipated when the settlement was negotiated? These are questions about how constitutional systems are designed to function, regardless of who holds their power.

Ordinarily, the government responds to the facts available when making a decision. Files are closed because the evidence no longer supports additional action, because legal deadlines have expired, or because the law otherwise requires it. Congress has also recognized that circumstances change. Statutes of limitations, exceptions for fraud, and other statutory mechanisms exist precisely because lawmakers understood that new evidence sometimes emerges after the government or the courts have concluded a matter.

The public record does not yet answer how the memo should operate if such circumstances were to arise. Unless it is litigated, it can be interpreted in many ways.

Every assertion of governmental authority should invite a corresponding question. What limits it?

That is one of the Constitution’s principal safeguards. Authority that cannot be clearly bounded is authority that becomes increasingly difficult to distinguish from discretion exercised solely according to the judgment of those temporarily entrusted with it. Put plainly, the strength of a constitutional system is measured not only by the powers it grants, but also by how clearly it defines their limits. And unclearly defined limits will inevitably be tested.

How far can the system be stretched?

If this analysis resonated with you, consider subscribing.

We examine the constitutional questions that outlast the news cycle, exploring how today’s decisions shape the balance of power, the strength of our institutions, and the precedents future generations inherit.

Sources:

“Two Major Trump Corruption Plots Revealed in Just 24 Hours,” The New Republic, June 29, 2026.

“Trump bought Axon stock before ICE sought $220M Taser contract,” Quartz, June 30, 2026.

“Trump, Lutnick’s sons stand to gain big profits from billion-dollar mining deal: report,” New York Post, June 29, 2026.

“FOREVER BARRED and PRECLUDED,” U.S. Department of Justice, May 19, 2026.

“Justice Department Announces Anti-Weaponization Fund,” U.S. Department of Justice, May 18, 2026.

“Settlement Agreement, Trump v. IRS (SDFL),” U.S. Department of Justice, May 18, 2026.

“Trump-IRS settlement ‘forever’ bars audits into tax claims for Trump and his family,” Reuters, May 19, 2026.

“Trump drops IRS lawsuit in exchange for DOJ $1.8 billion ‘weaponization’ fund,” Reuters, May 18, 2026.

“US judge temporarily blocks Trump’s $1.8 billion ‘weaponization’ fund,” Reuters, May 29, 2026.

“US judge indefinitely blocks Trump’s ‘anti-weaponization’ fund,” Reuters, June 12, 2026.

“Blanche says ‘anti-weaponization’ fund not moving forward,” Roll Call, June 2, 2026.

“Dems push to bypass Mike Johnson and outlaw weaponization fund,” Axios, June 25, 2026.

“Former IRS Contractor Sentenced for Disclosing Tax Return Information to News Organizations,” U.S. Department of Justice, January 29, 2024.

“IRS: Contractor leaked more than 400k returns,” Politico, February 25, 2025.

“Trump sues IRS, Treasury Department for $10 billion over tax return leak,” Reuters, January 29, 2026.

For what it's worth, this is a magnificent post.