Forever in Debt, Never at Home

Trump’s 50-Year Mortgage Doesn’t Fix the Housing Crisis. It Profits From It.

On November 8, 2025, Donald Trump posted a now-infamous image to his Truth Social account. It featured a side-by-side comparison: Franklin D. Roosevelt, credited with giving Americans the 30-year mortgage, and Trump himself, proposing a 50-year version. Bold, simplistic, and full of vintage branding flair, the post seemed designed to frame Trump as a housing visionary, a modern-day FDR who would unlock homeownership for millions.

Within hours, the backlash began.

Economists and housing experts denounced the idea as unserious, dangerous, and disconnected from the reality of today’s housing crisis. Troy Ludtka, senior economist at SMBC Nikko Securities, called it a “band-aid” on a supply problem. Gennadiy Goldberg of TD Securities pointed out that it would slow equity accumulation and entrench long-term debt. Sharon Cornelissen from the Consumer Federation of America was even more blunt: “The cost of that is that people won’t be able to build wealth through homeownership.”

Even Trump’s own administration seemed caught off guard. According to Politico, the White House was “blindsided” by the post. The idea had reportedly been floated to Trump by FHFA Director Bill Pulte — a politically connected heir to a homebuilding empire — who amplified the announcement himself shortly after, tweeting, “We are indeed working on The 50 year Mortgage — a complete game changer.”

This was not a policy rollout. It was a pitch and one that quickly unraveled under scrutiny.

Truth Social Post, November 8, 2025

Want to Know Your Rights?

Download a free digital copy of the U.S. Constitution—the same document Trump is trying to bulldoze. Learn exactly what he’s breaking… and how to fight back.

50,000 strong — and counting.

This Early Black Friday, become a paid subscriber for just $1 a week and help us keep the truth alive.

Join The Coffman Chronicle — $1/Week Early Access

A New Deal Rebrand With None of the Substance

By comparing himself to Roosevelt, Trump sought to position the 50-year mortgage as a transformative solution to the housing crisis, much as the New Deal introduced the 30-year fixed-rate loan during the Great Depression.

However, FDR’s mortgage reform was about systemic change: creating institutions (like the FHA), increasing supply, and stabilizing lending. Trump’s idea offers none of that. It’s not a new foundation, just a longer leash.

The logic behind the proposal is simple on the surface: extending the loan term from 30 to 50 years reduces monthly payments. That part is true, but misleading. Those lower monthly payments come with a steep cost, including far more interest over the life of the loan, painfully slow equity growth, and a mortgage that may outlive the borrower.

At best, a 50-year mortgage offers a kind of budget predictability. However, in almost every other way, it mirrors the worst parts of renting, while saddling homeowners with all the risk and none of the flexibility.

We’re Already Becoming a Renter Nation

To understand why this proposal falls flat, you have to understand the larger context. America has been slowly transitioning from a nation of homeowners to one of renters for decades. This is not by choice, but by necessity.

Home prices have exploded in recent decades. According to the U.S. Census Bureau, the median home price has increased from roughly $170,000 in 2000 to over $430,000 in 2025. Meanwhile, wages have lagged far behind, rising only incrementally after inflation adjustment. The result is a growing affordability gap that locks out even middle-income families.

Move.org

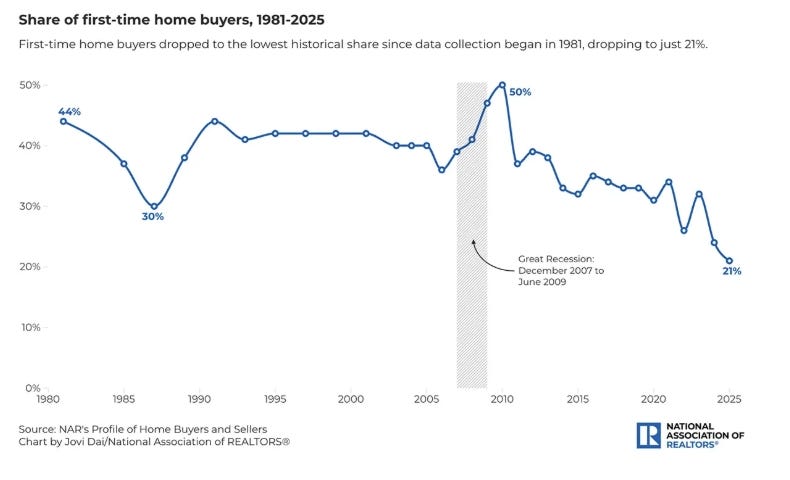

The median age of first-time homebuyers has now risen to 40, a record high. First-time buyers now make up only 21% of the housing market, a historic low. These statistics reflect a brutal truth: younger Americans are entering the market later, if at all. Many will never make it in at all. And if they do, under this proposal, they will be well past retirement age before they own their homes outright.

National Association of Realtors

They’re not just priced out. They’re competing against institutional investors who buy properties en masse, driving up prices and removing inventory from the market. In many regions, private equity firms, hedge funds, and REITs (real estate investment trusts) own substantial shares of single-family homes, homes that used to be available for working families.

We don’t have a housing shortage. We have a housing access crisis. The homes exist, but they’re being hoarded as investment assets rather than offered to the public.

This dynamic began to take shape after the 2008 subprime mortgage crisis, when millions of families lost their homes to foreclosure. Rather than those homes returning to individuals or families, many were scooped up in bulk by private equity firms and institutional investors, often at steep discounts. What began as a response to a crisis quickly became a business model: buy low, rent high, and hold. The effect was a historic transfer of property from working people to corporate portfolios, turning once-owner-occupied neighborhoods into profit centers.

The Illusion of Ownership

What the 50-year mortgage offers, then, isn’t ownership. It’s a long-term payment plan dressed up as empowerment.

Even assuming someone qualifies for a mortgage — which requires stable income, decent credit, and a significant down payment — they’ll likely spend the first 20–30 years paying mostly interest. If they move, refinance, or sell before the mortgage matures (as most homeowners do), they walk away with minimal equity and maximum debt.

And that’s if nothing goes wrong.

Unlike renters, homeowners are responsible for maintenance, property taxes, and insurance. Those lower monthly mortgage payments don’t include the cost of a broken furnace, roof repairs, rising premiums, or snow removal. Renters, frustrating as their position can be, aren’t on the hook when the water heater dies or the driveway cracks. They don’t have to budget for property taxes or shoulder the full burden of a natural disaster.

While a 50-year mortgage might offer a lower and more stable monthly payment than rent in some markets, it’s important to recognize what that number doesn’t include. Once you add the hidden costs of ownership, renting may actually be more affordable — and far less risky — for many.

The Real Beneficiaries

The longer the loan, the more money lenders make. A 50-year mortgage stretches the interest paid to near-predatory levels. It’s a rent-to-own scheme with no guarantee of ownership, and all the financial risk is shifted to the borrower.

If a homeowner defaults, the lender still owns the asset. If homeowners succeed, they’ll have paid two or three times the home's value over the life of the loan. Either way, the bank wins.

This proposal doesn’t address housing inequality. It doesn’t take on investor hoarding. It doesn’t offer public housing, rent stabilization, or down payment assistance. It simply offers the illusion of inclusion, and a longer, costlier path to a shrinking dream.

A Myth, Not a Model

The American housing system is broken, not because people stopped wanting homes, but because the system stopped making them accessible. Trump’s 50-year mortgage plan doesn’t fix that. It doesn’t empower people. It institutionalizes their struggle.

It’s not a ladder, but rather a treadmill. In the end, for most, it would not be ownership at all. It would be renting from the bank, with fewer protections and more risk.

It is no surprise that the people pitching it own multiple homes, have inherited generational wealth, power, and capital, and have likely never faced housing insecurity. Further, this proposal benefits those who already hold all the cards— home builders, banks, and lenders.

If this is the best we can offer, maybe it’s time to stop pretending homeownership is still the American Dream, and start asking why so many have been denied it in the first place.

Stay Informed. Stay Loud.

Subscribe to The Coffman Chronicle for no-BS political analysis, action guides, and daily truth bombs you won’t get from corporate media.

Sources:

“‘Band‑aid,’ ‘distraction’: Experts slam Pulte, Trump 50‑year mortgage idea” — Politico, Nov 10, 2025.

“Trump says 50‑year mortgages would be no ‘big deal’” — Reuters, Nov 11, 2025.

“50‑year mortgages? $2,000 tariff checks? What experts think of some of Trump’s unique policy ideas.” — PBS NewsHour, Nov 12, 2025.

“First‑Time Home Buyer Share Falls to Historic Low of 21 %, Median Age Rises to 40” — National Association of REALTORS® (NAR) press release, Nov 4, 2025.

“Top 10 Takeaways from NAR’s 2025 Profile of Home Buyers and Sellers” — NAR blog, Nov 3, 2025.

“The housing affordability crisis is so bad that the average American first‑time homebuyer is 40 years old” — Fortune, Nov 7, 2025.

“Home Values Have Increased by 68%—Can Income Keep Up” — Move.org, Apr 10, 2020.

“Young homebuyers lose more ground in housing market as states struggle to help” — Stateline, Nov 4, 2025.

| A guest post by

|

Absolute insanity - though homebuilders likely love it- more cash for them. Also winning: Banks. Losers? The rest of us.

Does he really think that's a good idea? It's like a prison. Then it won't just be houses that are inherited, but debts as well.