GOP to Big Banks: The CFPB Is Gone, Go Wild

🔹 Why Republicans Are Dismantling the Agency That Fights Financial Fraud

The first weeks of Donald Trump’s second term have already delivered a massive win for Wall Street and a devastating blow to American consumers. On February 1, 2025, Trump abruptly fired Consumer Financial Protection Bureau (CFPB) Director Rohit Chopra (WSJ), an outspoken regulator aggressively pursuing corporate wrongdoing. Within hours, Treasury Secretary Scott Bessent took control of the agency and froze nearly all its operations (Reuters), signaling that consumer protections are not a priority under Trump.

Meanwhile, Senator Ted Cruz and congressional Republicans had already launched a full-scale assault on the CFPB before the dismissal. On January 29, 2025, Cruz introduced legislation to completely defund the agency (Cruz.Senate.gov), aiming to strip its funding and render it powerless. If successful, this move would effectively dismantle the only federal watchdog designed to protect Americans from predatory financial practices. The motivations behind this attack are clear: Big banks and payday lenders have spent millions bankrolling Republican campaigns and are now cashing in their investment.

The Coffman Chronicle is powered by YOU—no billionaires, no corporate overlords. Help us keep exposing the BS, delivering sharp insights, and keeping you informed.

For just $8 a month or $80 a year, you can fuel the fight and be part of the movement.

Not ready to subscribe? No worries, chaos loves company, and you're always welcome. But if you’re fired up to keep us loud, proud, and unfiltered, smash that subscribe button now!

The CFPB: A Response to Corporate Greed

The CFPB was created in response to the 2008 financial crisis, which exposed the devastating impact of unregulated banking, reckless lending, and consumer fraud. Millions of Americans lost their homes, savings, and jobs due to Wall Street’s greed, while major banks received massive taxpayer-funded bailouts. In response, Congress passed the Dodd-Frank Act in 2010, creating the CFPB as an independent agency to hold financial institutions accountable and protect consumers from abuse.

Over the past decade and a half, the CFPB has secured over $17.5 billion in relief for consumers and exposed fraud at some of the nation’s largest financial institutions (Dodd Frank Update). Here are just a few of its most significant victories:

Wells Fargo Fake Accounts Scandal (2016 & 2022): The CFPB fined Wells Fargo over $3.8 billion for fraudulently opening fake accounts, charging illegal fees, and wrongfully repossessing homes and cars.

Navient Student Loan Settlement (2022): The agency secured $1.85 billion in relief for student borrowers misled by predatory loan practices.

Payday Lending Crackdowns: The CFPB has repeatedly sued payday lenders for trapping consumers in endless cycles of debt.

Bank of America Illegal Fees (2023): A $250 million penalty for charging duplicate fees, withholding credit card rewards, and opening unauthorized accounts.

Zelle Fraud Investigation (2024): The CFPB exposed rampant fraud on the Zelle payment platform and forced major banks to take accountability.

In short, the CFPB has been one of the few government agencies willing to take on corporate misconduct head-on. That is precisely why Trump and his allies want it gone.

Ted Cruz’s Defunding Plan: A Handout to Wall Street

Senator Cruz’s “Defund the CFPB Act” bill aims to strip the agency of all funding by cutting off its revenue from the Federal Reserve, effectively shutting it down without repealing Dodd-Frank.

Cruz, echoing longtime GOP talking points, called the CFPB “an unelected, unaccountable bureaucratic agency” that has imposed “burdensome regulations” on businesses. However, Cruz and his colleagues refuse to acknowledge that these regulations protect everyday Americans from the financial abuses that triggered the last economic meltdown.

So why is Cruz so eager to dismantle the CFPB? Follow the money.

Wall Street’s Millions Flow to the GOP

The financial industry has long been one of the biggest donors to Republican campaigns, and this election cycle was no exception. In 2024 alone, Wall Street banks, payday lenders, and hedge funds funneled over $200 million to GOP candidates and PACs (Dodd Frank Update)—many of whom are now leading the charge to kill the CFPB.

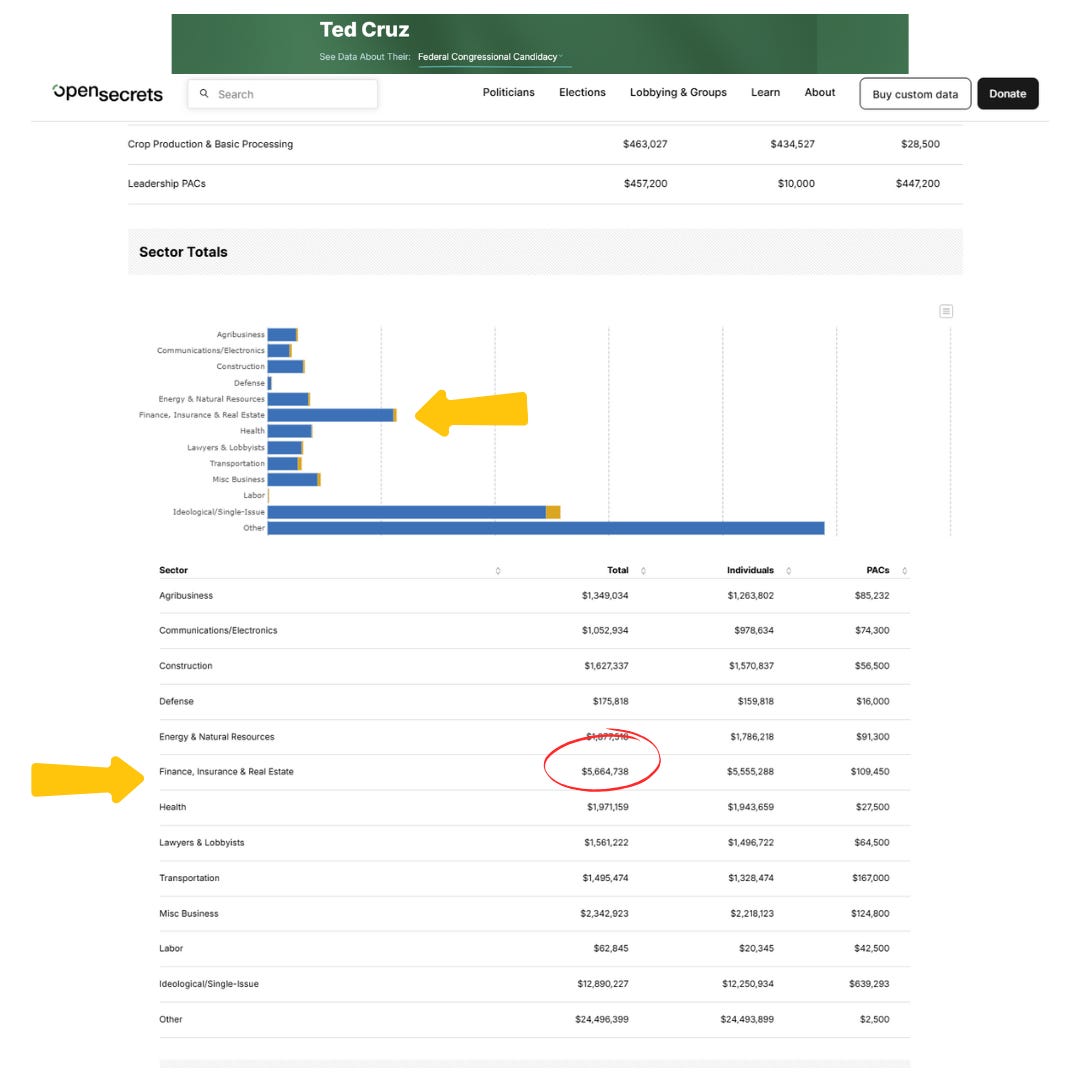

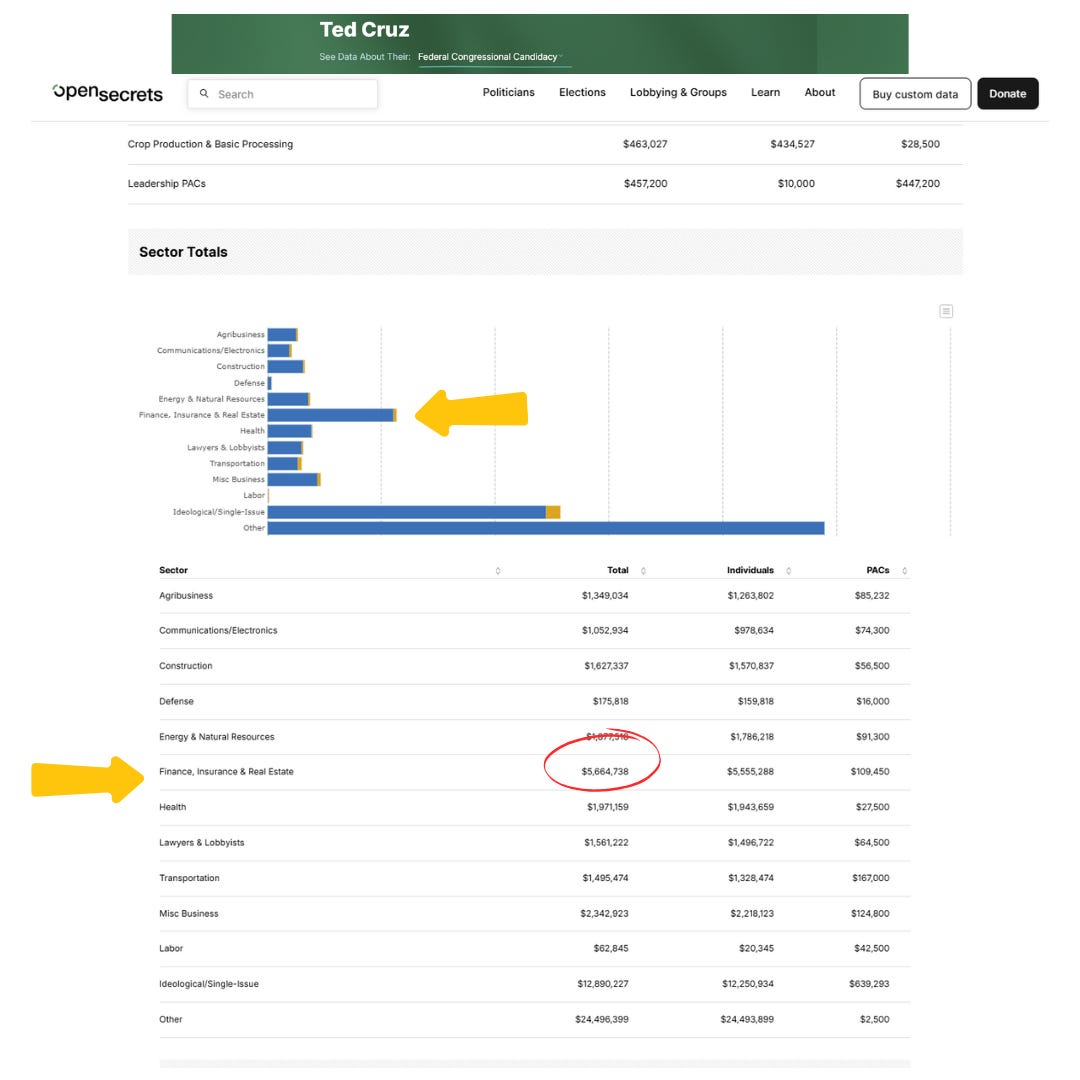

Ted Cruz received over $5 million from the Finance, Insurance, and Real Estate Sector.

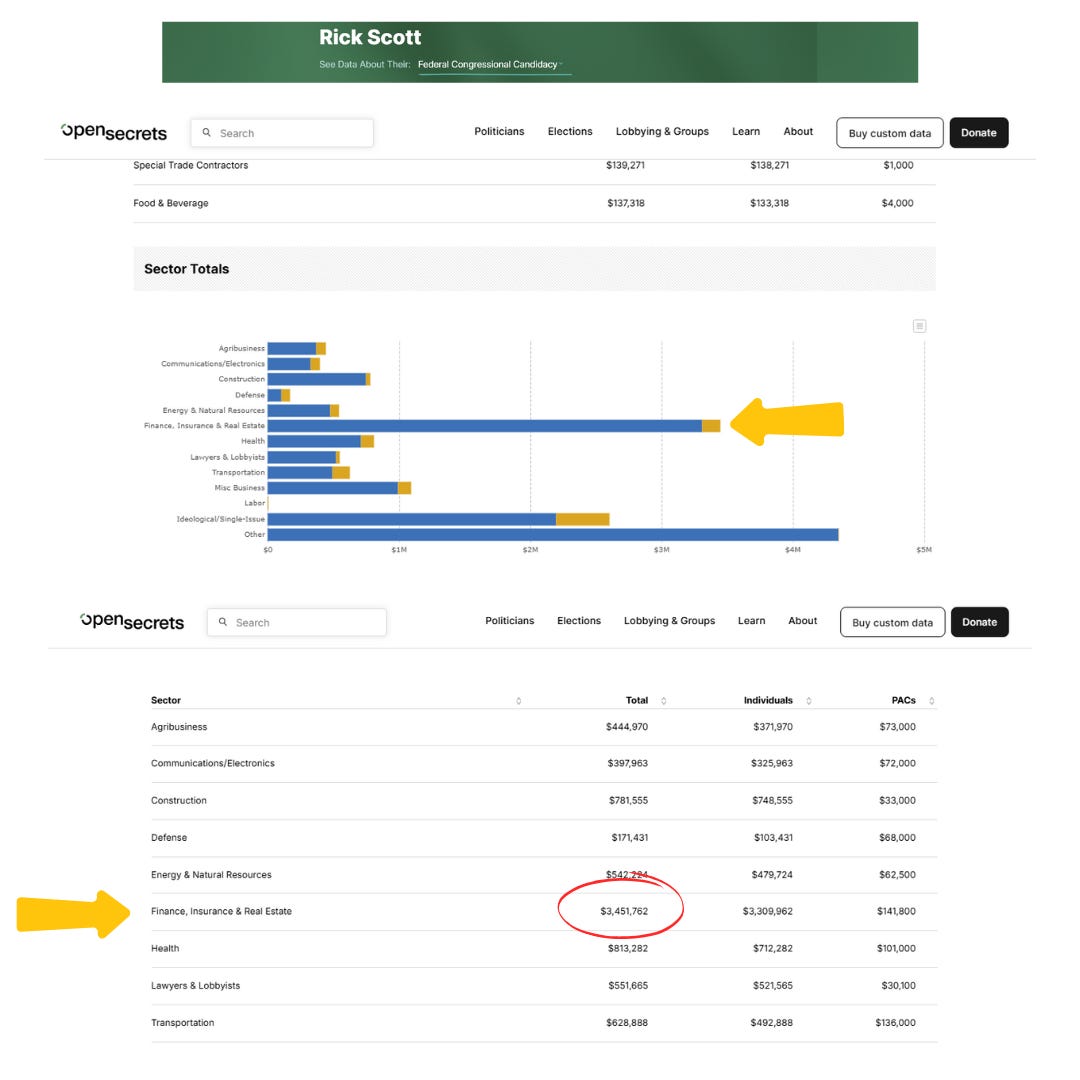

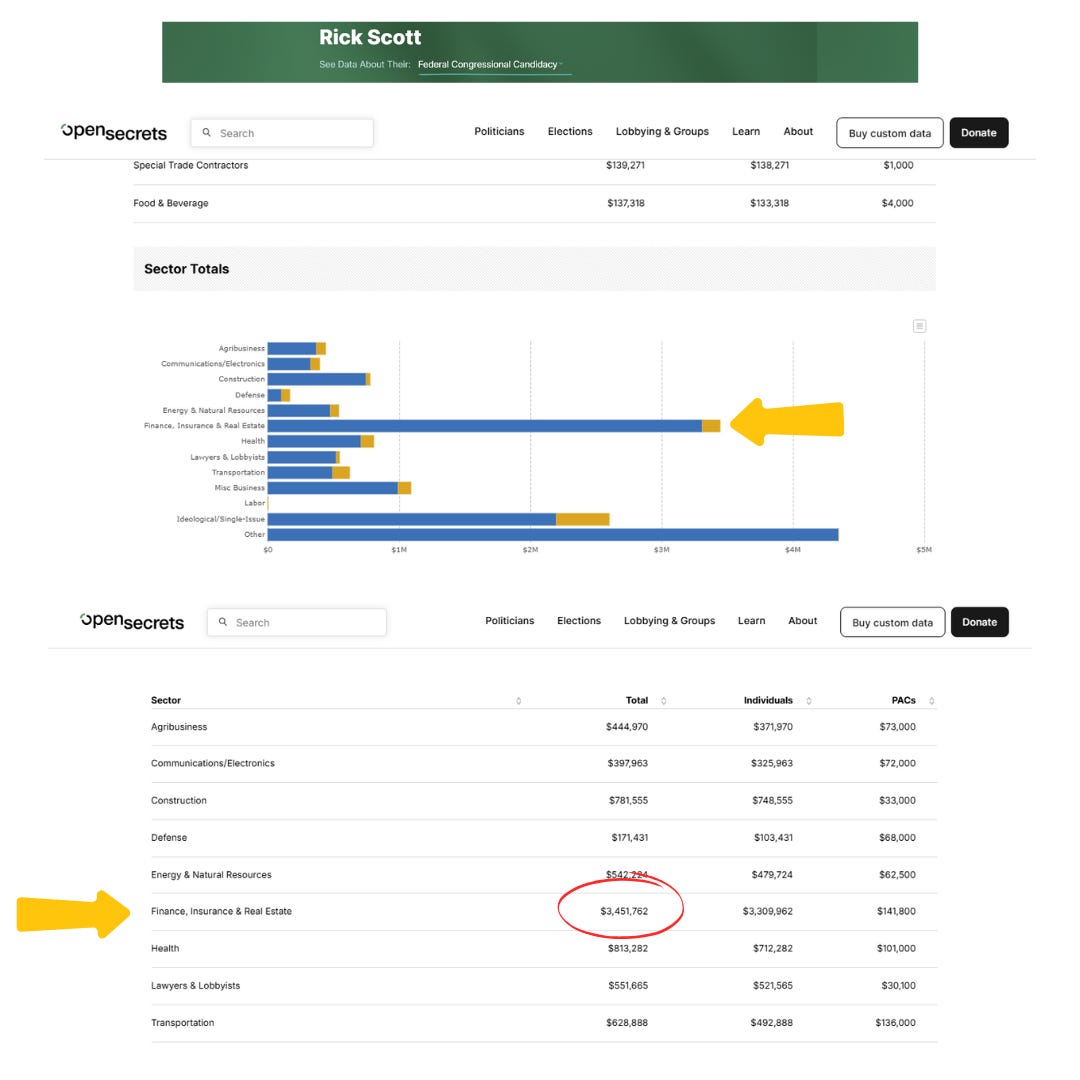

Senator Rick Scott, another supporter of the defunding bill, took nearly $3.5 million from Finance, Insurance, and Real Estate.

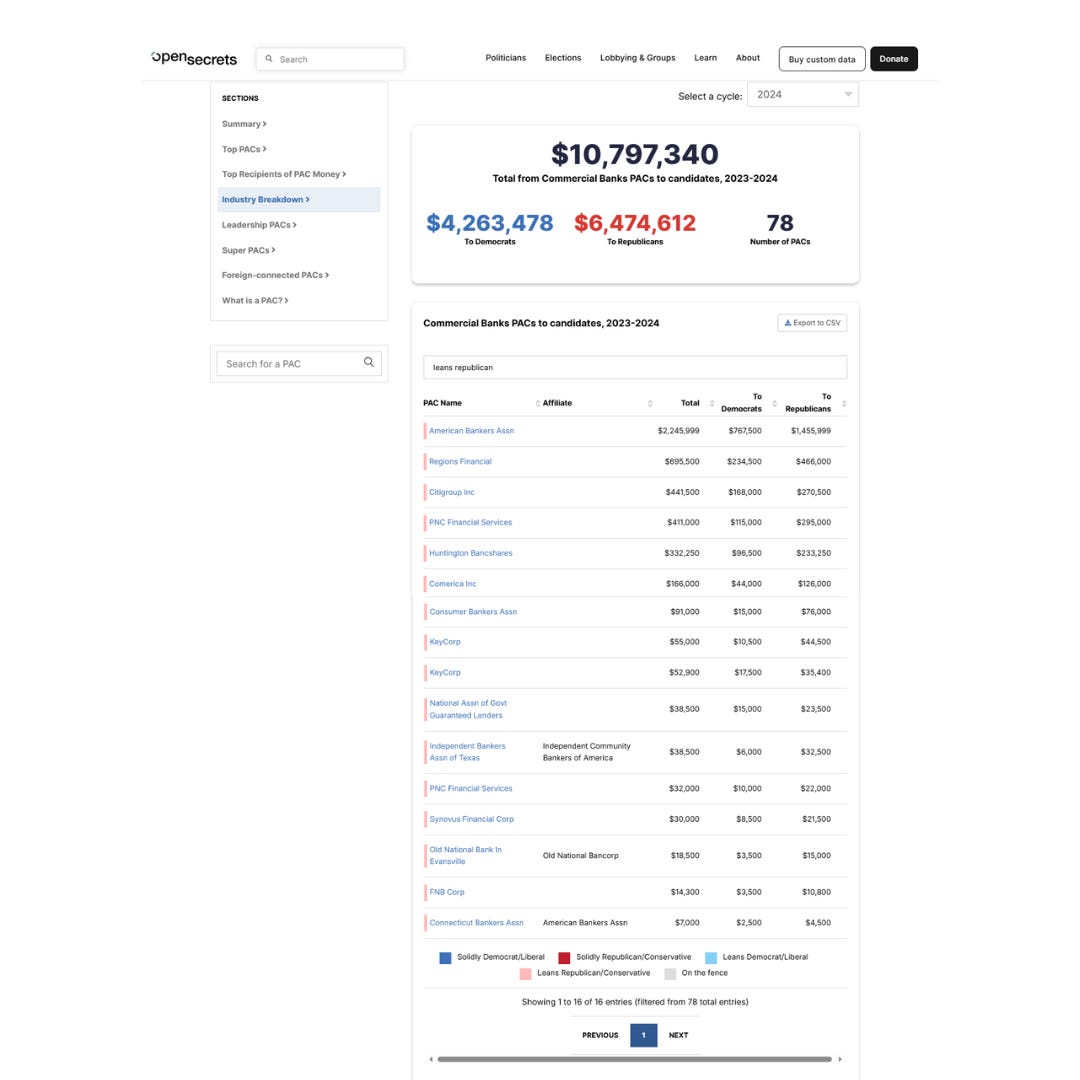

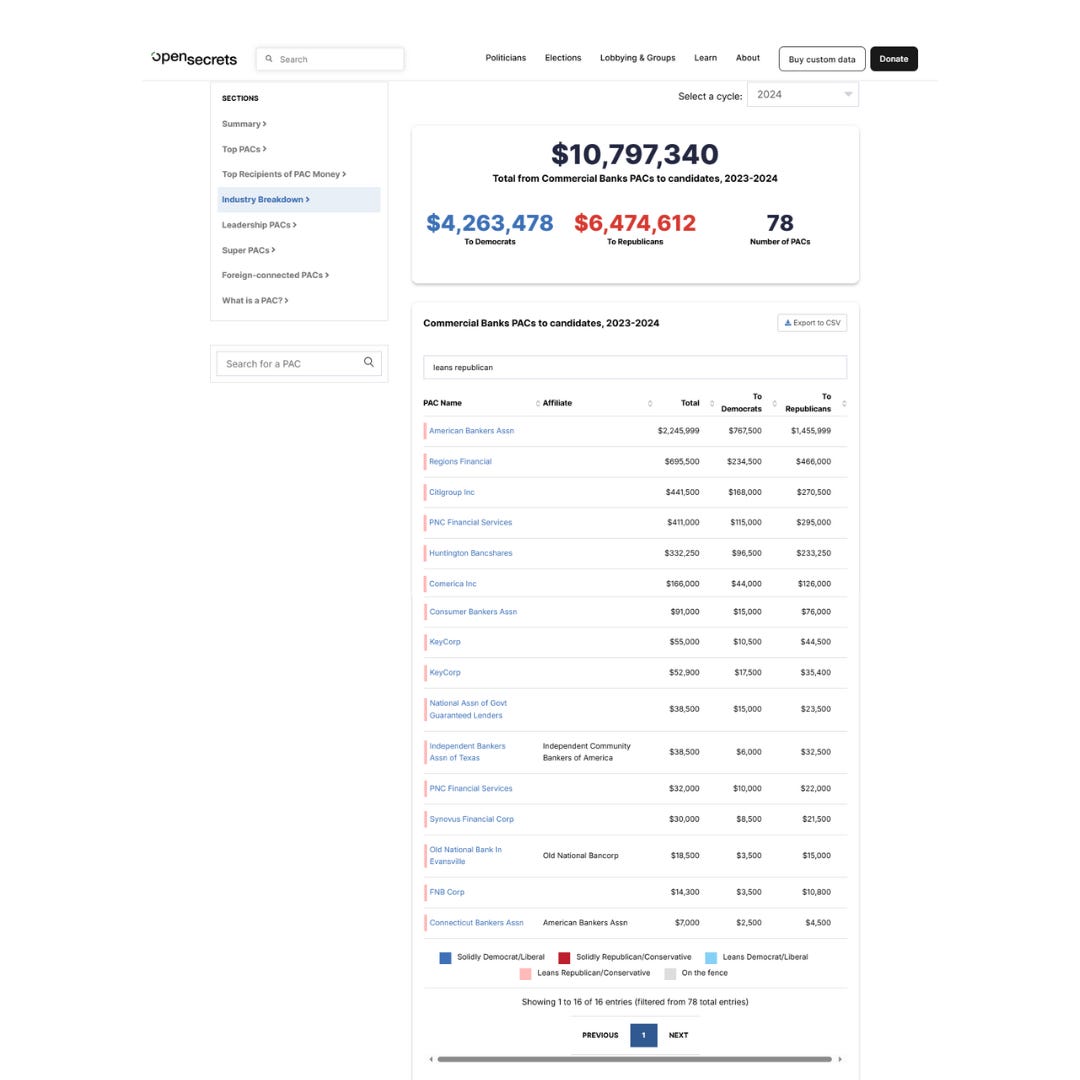

Republicans overall received over $6 million from Commerical Bank PACS alone.

Simply put, this is a return on investment for Wall Street. Banks don’t donate millions out of the goodness of their hearts—they expect policy favors in return. And what bigger favor could they ask for than eliminating the very agency that holds them accountable?

What Happens If the CFPB Is Defunded?

If Cruz’s bill passes, consumers will be left entirely defenseless against corporate financial abuse. Here’s what’s at stake:

❌ Banks will have free rein to impose hidden fees, predatory loans, and fraudulent account practices—with no risk of federal enforcement.

❌ Payday lenders will once again be able to trap low-income Americans in cycles of debt, charging interest rates as high as 400%.

❌ Credit card companies could bring back abusive billing practices, burying consumers in skyrocketing fees and penalties.

❌ Debt collectors will have fewer restrictions on harassment, wage garnishment, and fraudulent debt claims.

This isn’t just speculation—it’s exactly what happened before the CFPB existed. Without an independent consumer watchdog, Wall Street and predatory lenders will once again be free to exploit working families with impunity.

The Bottom Line

The Republican push to dismantle the CFPB isn’t about “government overreach” or “freedom.” It’s about money and power. Trump, Cruz, and their allies are doing the bidding of the very financial institutions the CFPB was created to rein in—and consumers will pay the price.

And let’s be real. Money in politics is a major problem on both sides. Both parties receive substantial financial backing and policy influence from corporations, industries, lobbyists, and special interests. Meaningful reform is essential to restoring faith in our democratic processes.

Right now, the question is whether the American people will fight back against defunding before it’s too late. If we allow the CFPB to be gutted, we won’t just be rolling back regulations—we’ll be handing big banks a blank check to exploit us once again, and further efforts to get money out of politics will be pointless.

Defunding/ending the CFPB would be devastating. Consumers will lose - big banks, payday predators, and credit card companies will win- and by win, I mean, they will extract cash in the most painful ways and will face zero chance of being held accountable.

I watched all the garbage play out in 2006...Chase even tried to corner me to submit to an **ILLEGAL INTEREST RATE INCREASE ON MY FIXED MORTGAGE INTEREST RATE!!!** I instantly REFINANCED with a small local bank, & moved my accounts to that small local bank. Chase was as bad as Wells Fargo & Bank of America!!! I dumped all those big banks. I deal ONLY with small local banks. I won't even have a credit card with them...mine are all with the small local banks that have no connection to the bigger Wall Street banks... IF I TOLD YOU HOW WALL STREET ACTUALLY GOT IT'S NAME, YOU'D BE HORRIFIED!!!- CAN LOOK IT UP YOURSELF THROUGH SYRACUSE UNIVERSITY NATIVE STUDIES ARCHIVES...YUP ...THE ORIGINAL DUTCH COLONY NEW AMSTERDAM ERRECTED A PALISADE FENCE ALONG WHAT TODAY IS WALL STREET, TO PROTECT THE COLONY FROM AN INEVITABLE ATTACK BY NATIVE TRIBALS IN RETALIATION FOR THE DUTCH SLAUGHTERING HUNDREDS OF TRIBALS, & BRINGING BACK THE HEADS OF THOSE DEAD INDIANS TO KICK DOWN THE THEN COBBLESTONE STREET THAT BECAME WALL STREET!!! NICE HISTORY YA BASTARDS!!! WE'RE NOT DEAD YET!!!!!