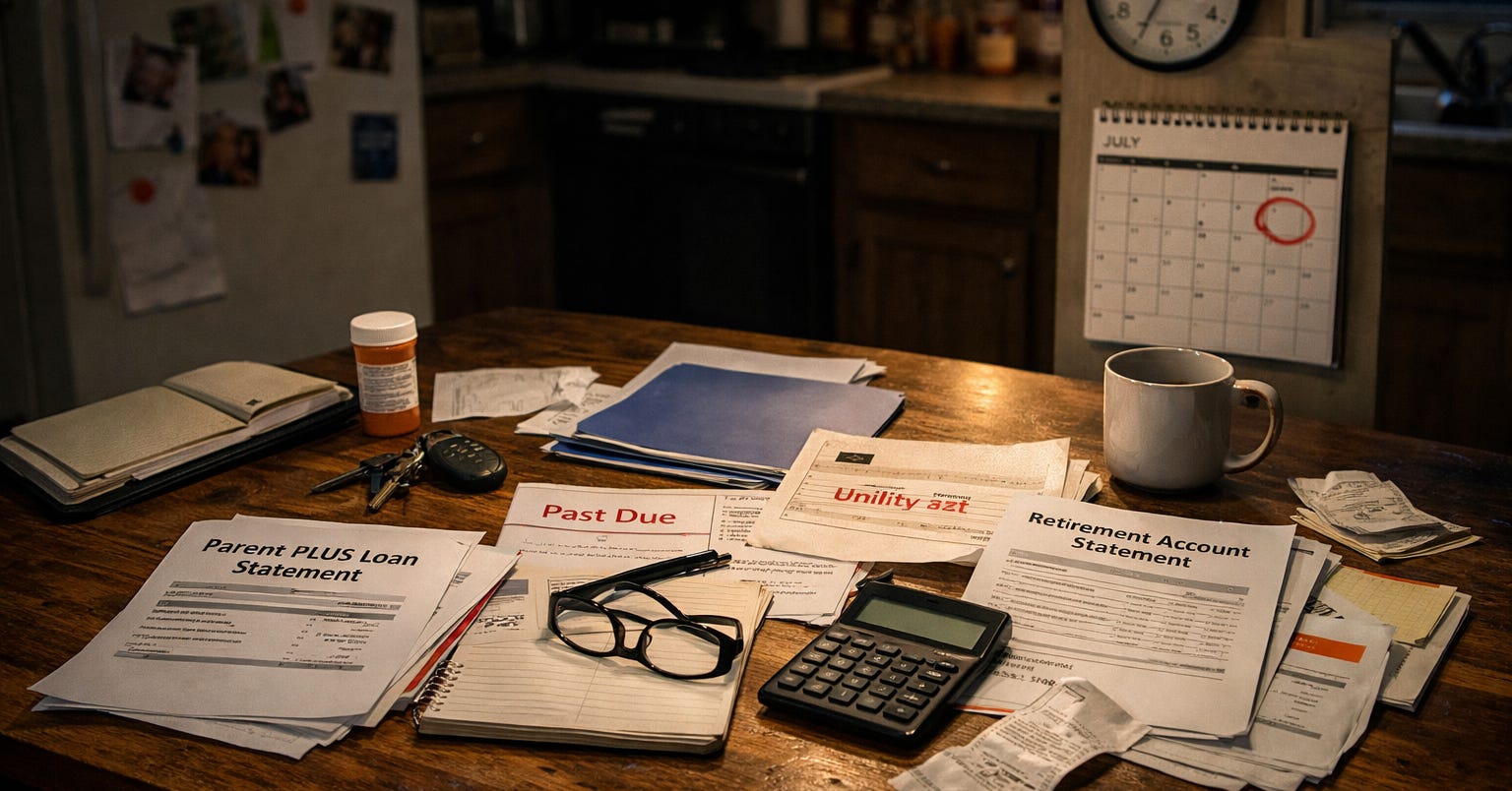

The Parent PLUS Trap: How College Debt Can Steal a Parent’s Retirement

For many families, one missed administrative step can mean higher payments, fewer protections, and years of delayed retirement.

Parent PLUS loans were supposed to be a bridge. A way for parents to help their children reach college, opportunity, and a more stable future. But for too many families, that bridge has turned into a trap. What looked like a sacrifice on the front end can become a financial ambush on the back end, especially for parents nearing retirement who discover too late that these loans do not carry the same repayment protections many people assume federal student debt does.

That is the danger at the center of this story. If you have Parent PLUS loans and have not consolidated them, you may be shutting yourself out of the income-driven repayment options that can make those loans manageable. That sounds technical. It is not. It is the difference between a payment shaped by your real income and a bill that can bulldoze the years when you were supposed to be catching up on savings, paying down your last debts, and preparing to leave the workforce with some dignity intact.

That is what makes Parent PLUS different from the way most people think about student loans. The debt does not just follow the student. It follows the parent, often into middle age and beyond. It follows them into years marked by rising medical costs, stagnant wages, and shrinking retirement windows. One bureaucratic step can determine whether this debt remains survivable or becomes one more reason you have to keep working long after you thought you would be done. This is not just a loan issue. It is a retirement trap disguised as parental help.

This Community Is Powered by You

What started as a small circle has grown into something much bigger, and it’s all because of readers like you.

Every time you forward this email, post it on socials, or bring someone new into the fold, you’re helping build one of the most passionate, independent political communities out there.

Want to keep the momentum going?

Share this newsletter with someone who should be part of this conversation.

Thank you for being here. It means everything.

The Rule Most Parent PLUS Borrowers Never Hear

The problem starts with a detail most families are never clearly warned about: Parent PLUS loans do not come with the same repayment protections many people associate with federal student debt. On their own, they do not qualify for the full menu of income-driven repayment plans many borrowers now assume are a standard federal safety valve.

That is where consolidation enters the story, and why it matters so much. Consolidation is not magic. It has tradeoffs. It can stretch repayment out longer and increase the total interest paid over time. But for many Parent PLUS borrowers, it is the gateway to the only income-driven repayment plan the system currently offers. Without that step, many parents are left with fewer options and harsher monthly realities.

This is the part that should make people angry. The loan was sold as a way for parents to help open a door for their children. But buried in the repayment rules is a system that can punish that decision years later, long after the tuition bills were paid and long after the child left campus. A parent can spend years assuming they have the same protections as other federal borrowers, only to discover that one loan category and one missed administrative step leave them with far fewer options than they thought.

That is not a minor paperwork problem. That is the architecture of a debt trap.

And that is why this story is not really about forms. It is about timing, information, and power. If a borrower does not know consolidation is the gateway, they can lose years in the wrong repayment structure before they even understand what happened. For a parent already in middle age or heading toward retirement, those lost years matter. They are the years when savings are supposed to grow, not be swallowed by a loan program marketed as help.

The Deadline Story Is Real, Even If It Is Not What People Think

This is where the confusion starts. There is no single, simple federal warning telling every Parent PLUS borrower to consolidate by a single, universal date or lose every income-driven option forever. That is not the clean, dramatic countdown many people imagine.

The real problem is quieter than that. Every month a borrower stays in an unconsolidated Parent PLUS loan is another month outside the repayment structure, which may lower the bill to something more manageable. That is still a deadline story. It is not measured by a single flashing date on the calendar. It is measured in lost flexibility, lost options, and lost time.

There is, however, a separate set of very real calendar dates tied to the broader July 2026 Parent PLUS changes. That matters because it shows the policy landscape around these loans is tightening, not loosening. The direction is clear: more limits, more complexity, more pressure on families already trying to hold everything together.

That is the point readers need to hear. There may not be a single universal consolidation deadline stamped across all Parent PLUS accounts, but delay is still dangerous. Delay can leave borrowers trapped in the wrong repayment structure, and once a family falls behind, catching up can get expensive fast. This is exactly the kind of bureaucratic trap that does not feel urgent until the bill arrives and the damage is already underway.

When a Loan Follows You Into Retirement

This is the part policymakers and loan servicers can explain in charts and tables, but families feel in real life. A Parent PLUS loan does not sit neatly in an abstract category called educational debt. It shows up in the grocery bill. It shows up in the monthly budget meeting at the kitchen table. It shows up when a parent who thought the hardest years were behind them realizes they are still carrying a bill that does not care how close they are to retirement, how much their prescriptions cost, or how little room is left in the household budget.

That is why consolidation matters so much. Yes, it can mean paying longer. Yes, it can mean more interest over time. But for many older borrowers, the immediate issue is simpler and harsher than that: can the monthly payment be brought down to something they can actually live with? That is the tradeoff. The payment may become more survivable, but the debt can stretch deeper into the years when people had hoped to be done working.

For a younger borrower, a longer repayment horizon is bad enough. For a parent in their fifties or sixties, it can be devastating. These are the years when people are supposed to be catching up on retirement savings, paying off the mortgage, helping aging relatives, or managing rising medical costs. Instead, many are stuck doing math they never expected to be doing this late in life: How many more years can I keep working? How much longer can I postpone retirement? What gets cut first if this payment does not come down?

That is where it stops being a student-loan story and becomes something bigger. It becomes a story about the way America shifts risk downward. Colleges get paid. The system moves on. And the parent is left carrying the debt into the years when their own financial runway is getting shorter, not longer.

Parents were told this borrowing was about giving their children a better future. What they were not told clearly enough was that the debt could come back years later and start eating away at the future they were trying to protect for themselves.

The Bureaucracy Is Part of the Trap

What makes this story so infuriating is that the danger is not obvious when families are signing the paperwork. Parent PLUS sounds like aid. It sounds like a public program meant to help parents fill a gap so their child can stay in school. What it does not sound like is a loan category with narrower repayment options, technical barriers to relief, and consequences that can spill into the last working years of a parent’s life.

But that is exactly what the rules have created.

That is how bureaucratic design becomes financial punishment. The people most likely to get hurt are not the people with accountants, planners, and attorneys walking them through every repayment scenario. They are working and middle-class families doing what the system told them to do: borrow to keep the child in school, trust that federal loans come with federal protections, and assume the details can be sorted out later. Then later arrives, and the fine print matters more than the promise ever did.

The larger pattern here is hard to miss. More and more Americans are living inside systems where one missed form, one misunderstood rule, or one delayed administrative step can trigger years of damage. Parent PLUS fits that pattern perfectly. It takes a parent’s act of sacrifice and runs it through a maze of eligibility rules that many borrowers do not even know exist until the bill becomes impossible to ignore.

That is not just bad communication. It is a policy choice. It is a policy choice to build a program that invites parents to borrow tens of thousands of dollars and then ties manageable repayment to technical steps many families do not understand until much later. It is a policy choice to place that burden on aging parents rather than design a simpler, more transparent path from the start.

This Was Supposed to Help Families, Not Trap Them

The simplest truth in this story is still the most damning one. Parent PLUS was supposed to help parents support their children’s education. For too many borrowers, it has instead become a late-life debt burden with rules most people never fully understood when they signed up. And because these loans do not come with the same repayment protections many borrowers assume, the cost of not consolidating can land at exactly the worst possible time: when parents are trying to stabilize their finances, protect what savings they have left, and prepare for retirement with some dignity intact.

That is why this is not just a student-loan article. It is a retirement article. It is an article about how a parent’s attempt to help a child can turn into years of extra work, delayed plans, and financial stress that were never part of the bargain.

If there is one takeaway you should remember, it is this: the trap is not just the debt itself. The trap is the combination of debt, fine print, and delay. In a program like Parent PLUS, delay can get expensive fast. And when that delay collides with the last working years of a parent’s life, the cost is not theoretical. It is measured in postponed retirement, drained savings, and time people do not get back.

This was supposed to be a bridge for families. Too often, it becomes a burden parents carry right up to the edge of retirement.

Support Independent Media

The Coffman Chronicle exists to connect policy to the kitchen table, expose the systems that shift pain downward, and tell the truth about who pays when Washington’s fine print collides with real life.

If this kind of independent journalism matters to you, and you can afford to support it, please consider becoming a paid subscriber.

Sources:

“Direct PLUS Loans for Parents.” StudentAid.gov. Accessed April 1, 2026.

“Income-Driven Repayment (IDR) Plans.” StudentAid.gov. Accessed April 1, 2026.

“Top FAQs About Income-Driven Repayment Plans.” StudentAid.gov. Accessed April 1, 2026.

“What Options Exist for Paying Back Direct PLUS Loans?” StudentAid.gov Help Center. Accessed April 1, 2026.

“5 Things to Know Before Consolidating Federal Student Loans.” StudentAid.gov. Accessed April 1, 2026.

“Direct Consolidation Loan Application.” StudentAid.gov. Accessed April 1, 2026.

“Reimagining and Improving Student Education.” Federal Register, January 30, 2026.

This would be a very helpful article to those adults with children and grandchildren that they want to help finance through college. I am 83 now, and my parents helped us with our 3 children's education with something called a Clifford trust-not even sure they have those any more. We are helping our 7 grandchildren using 529 accounts that I set up for them when each was born, and that has worked out very well. In case there are any others out there who want to help their grandkids without sabotaging their own retirement.