The Subsidy Vote That Came Too Late

House Republicans join Democrats to extend ACA subsidies, but the damage is already done

On January 8, the House of Representatives passed a bill to extend enhanced Affordable Care Act premium subsidies for three more years. Seventeen Republicans crossed the aisle to join every House Democrat in supporting the bill, which cleared the chamber 230 to 196.

The vote was framed by many as a breakthrough, a moment of bipartisanship on healthcare after months of gridlock. A few Republican members defied their leadership and delivered a win for policy over partisanship. However, by the time the votes were cast, the subsidies had already expired. Premiums have gone up, open enrollment closes in less than a week, and millions of Americans are already deciding whether they can afford insurance in 2026.

The question now is not just what happens in the Senate, but what happened in the House over the past year to let it get to this point at all, and, crucially, what’s next.

Tasos Katopodis/Getty Images for DNC

Want to Know Your Rights?

Download a free digital copy of the U.S. Constitution, the same document Trump is trying to bulldoze. Learn exactly what he’s breaking, and how to fight back.

100,000+ strong — and counting.

This winter, become a paid subscriber for just $1 a week and help us keep the truth alive.

Join The Coffman Chronicle — $1/Week

How the subsidies expired

The enhanced subsidies at the heart of this debate were originally part of the American Rescue Plan in 2021 and extended under the Inflation Reduction Act. They lowered premiums for millions of Americans by expanding eligibility and increasing the amount of aid available through ACA exchanges. However, they came with an expiration date: December 31, 2025.

Congress had multiple opportunities to act before the deadline. The most obvious and recent were during the fall 2025 budget negotiations and the continuing resolution (CR) that followed.

Yet in both cases, the extension was blocked. The budget process broke down as House Republicans under Speaker Mike Johnson refused to include the subsidy extension in the overall funding package. When the fiscal year began on October 1 without an agreement, the government entered a shutdown. It would last 43 days, making it the longest in American history.

Even then, the opportunity was still on the table. When the shutdown finally ended on November 12 with a short-term CR, Republican leadership again left out the ACA subsidy extension from the deal. The final bill passed with controversial low-level bipartisan support, but it was merely a clean funding resolution, with no healthcare policy provisions. The subsidies expired, and the budget was kicked down the road again.

The last-minute reversal

While the procedural break came in December, the political tension began much earlier. As early as September, a handful of House Republicans raised concerns about the looming expiration of ACA subsidies. Members like Brian Fitzpatrick of Pennsylvania and Mike Lawler of New York quietly pushed for an extension to be included in the House GOP’s broader health care legislation. Their proposals were rejected by party leadership.

When the government shut down on October 1, those concerns grew louder, but not more forceful. As the shutdown dragged into November, some Republicans continued to press for action on subsidies, yet none drew a public red line. When the continuing resolution finally passed on November 12 — without the subsidy extension — they still voted for it.

It wasn’t until December that a real break occurred. On December 14, nine Republicans signed a discharge petition launched by Democrats to force a floor vote on the subsidy extension. The members — Mike Lawler (NY-17), Brian Fitzpatrick (PA-01), Rob Bresnahan (PA-07), Ryan Mackenzie (PA-08), Tom Kean Jr. (NJ-07), Marc Molinaro (NY-19), John Duarte (CA-13), David Valadao (CA-22), and Anthony D’Esposito (NY-04) — defied leadership to give the bill a path forward.

It worked. On January 8, the bill came to the floor. Seventeen Republicans voted in favor, including the original nine.

It was a meaningful moment. However, it wasn’t the first, nor was it enough to undo the consequences of waiting.

When the vote no longer mattered

Even with the House finally acting, it’s too late to make a meaningful difference for 2026.

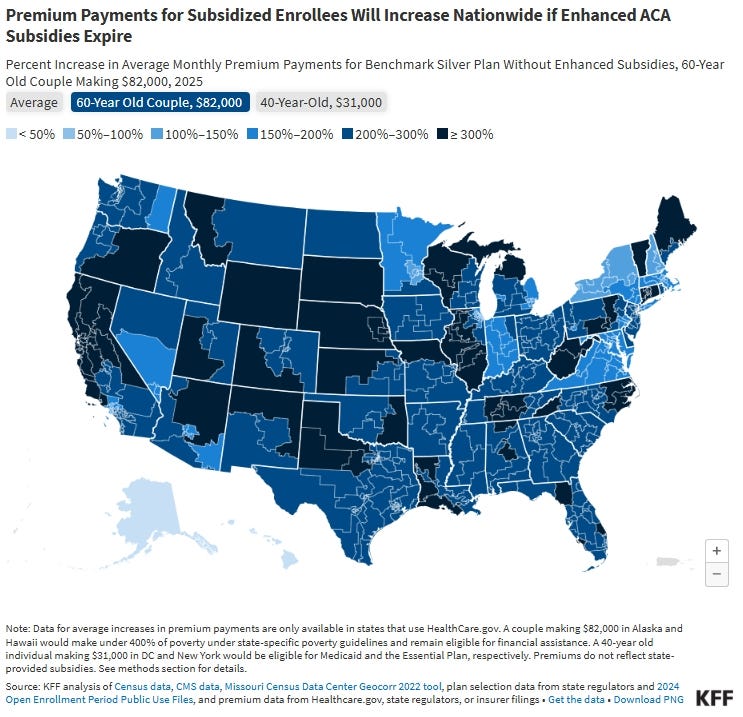

Open enrollment ends January 15 in most states. Insurers have already priced and finalized plans based on the assumption that subsidies were expiring. For most consumers, the premium changes have already taken effect. At best, a successful extension — if passed by the Senate and signed into law — might result in tax credit adjustments after the fact. However, that’s little comfort to people who made their enrollment decisions this month.

Source: KFF

The system doesn’t adjust instantly. Even retroactive fixes take time to implement. For most Americans buying coverage on the exchange, the reality is already locked in: they are paying more in 2026.

The Senate’s next move

The bill now moves to the Senate, where its future is uncertain. Republicans have already signaled they want changes, including not extending the subsidies for three years, but perhaps only for two. Some want income caps reinstated. Others are pushing for tighter eligibility checks and what they’re calling “fraud assurances.”

It’s a familiar move. Delay the fix. Muddle the terms. Shift the debate.

What their concerns fail to address is the evidence about fraud in the ACA marketplace, which tells a different story.

Where the real fraud lies

Most fraud accusations in the ACA marketplace are not about individual applicants scamming the system. They’re about brokers and insurers manipulating enrollment, steering consumers toward high-commission plans, or failing to report when people leave coverage so they can keep collecting subsidies.

Despite years of politically motivated investigations, there is no serious data suggesting widespread fraud by enrollees. Unsurprisingly, however, Republicans aren’t demanding safeguards against insurance industry abuse. They’re asking for more barriers between people and coverage.

And while they claim to care about fraud now, the record shows otherwise.

Who gets a pardon

The contrast between today’s fraud rhetoric and recent presidential actions is hard to ignore.

Across both of his administrations, Donald Trump has repeatedly intervened on behalf of people convicted of large-scale insurance and healthcare fraud, cases involving not paperwork errors or marginal abuse, but hundreds of millions and billions of dollars.

Trump1.0 pardons

In December 2020, during the final weeks of his first term, Trump commuted the sentence of Philip Esformes, who had been convicted in 2019 of orchestrating what federal prosecutors described as the largest Medicare fraud scheme in U.S. history. The case involved roughly $1 billion in false claims, kickbacks, and money laundering tied to nursing homes and assisted living facilities. The commutation left the conviction intact but reduced the prison term drastically.

Trump also intervened in the case of Sholam Weiss, whose crimes contributed to the collapse of National Heritage Life Insurance Company in the late 1990s. The fraud drained approximately $450 million, wiping out policyholders and destabilizing an entire insurer. In January 2021, on his final full day in office during his first term, Trump granted a full pardon. Weiss had been sentenced to 845 years in prison — one of the harshest sentences ever handed down for white-collar fraud. The pardon was issued over objections from the Department of Justice and without requiring restitution.

Trump2.0

In 2025, during Trump’s second term, he pardoned Robert Harshbarger Jr., a pharmacist convicted of healthcare fraud involving the substitution of unapproved drugs in place of FDA-approved medications. Harshbarger is the husband of a sitting Republican member of Congress. The pardon eliminated remaining penalties and restitution obligations.

These are not isolated or minor cases. They span two administrations, involve vast sums of public money, and center on corporate or professional actors operating inside the healthcare and insurance system.

That context matters when lawmakers now insist that any ACA subsidy extension must come with “fraud assurances.” The same political ecosystem demanding new barriers for patients has repeatedly extended mercy to people whose crimes dwarfed anything alleged in the ACA marketplaces. When fraud is committed at scale, by powerful actors, the response has often been clemency. When fraud is discussed in the context of health insurance access, the focus shifts downward, toward applicants, paperwork, and eligibility.

The message is not subtle. Fraud is treated as forgivable when it is expensive, complex, and committed by the well-connected. It becomes urgent only when it can be used to justify restricting access for everyone else.

The wrong fight

The same week the House passed the ACA subsidy extension, Trump’s Justice Department launched a new national anti-fraud initiative. It is not to pursue insurers, nor to investigate brokers. Instead, it aims to investigate daycare centers in Minnesota in response to a widely discredited viral video from YouTuber Nick Shirley.

The DOJ is now devoting federal resources to chase stories that have already collapsed under basic scrutiny. Meanwhile, the actual drivers of insurance fraud go untouched.

What we’re left with

There is movement in Congress to address the ACA subsidy expiration. That matters. The discharge petition was real. The House vote was real. Some members did put their seats on the line. Voters should remember that.

However, we should also remember what happened before the vote, when these same lawmakers had the opportunity to include the extension in the budget or in the continuing resolution, as a condition of ending the shutdown. They didn’t hold the line. They went along with party leadership, and millions of Americans are paying the price.

This isn’t a story of courage. It’s a story of consequence.

Even if the Senate passes the bill, even if it’s signed into law, it won’t help people this year. Moreover, it won’t address the real sources of fraud. That’s the cost of waiting. We will pay in lives, in untreated conditions, and in worsening health outcomes.

If you found this analysis useful, consider subscribing to stay informed on the policy fights that shape real lives. We break down what’s happening in Washington, and what’s being buried — with clarity, context, and no shortcuts. You deserve the full story.

We are here to provide it.

Sources:

“17 House Republicans vote with Democrats to extend Obamacare subsidies for 3 years” — ABC News, January 8, 2026

“House votes to extend ACA subsidies, eyes turn to Senate” — The American Journal of Managed Care, January 8, 2026

“Discharge petition” — Wikipedia

“House to vote on ACA subsidies extension after 9 Republicans help get it to the floor” — ABC7 New York, January 7–8, 2026

“House passes bill to extend health care subsidies in defiance of GOP leaders” — PBS NewsHour, January 8, 2026

“GOP Rebels Deliver Sharp Rebuke of Johnson on Health Care” — The Daily Beast, January 8, 2026

“Trump’s pardons included health care execs behind massive frauds” — PBS NewsHour, January 22, 2021

“Trump Says He’ll Stop Health Care Fraudsters. Last Time, He Let Them Walk.” — KFF Health News, April 1, 2025

“Philip Esformes” — Wikipedia

“Sholam Weiss” — Wikipedia

The biggest fraudster in the larger scheme is Donald Trump and some of his Trump/ Republican cult following. His pardons of past insurance executives indicted and in jail for their large scale fraud have not been largely shared with the public. My biggest concern is that behind the scenes manipulation and gerrymandering will jeopardize a free and honest election and limit or stop the public backlash that will present in the spring and fall of this year!

I thought this is actually a good developement. Now i’m not so sure about it.

Thank you for explanation.