The Credit Card Crisis Is the Affordability Crisis With Interest

Americans are not just swiping for luxuries. Millions are using credit cards to survive, and banks are turning household pressure into interest income while Congress looks the other way.

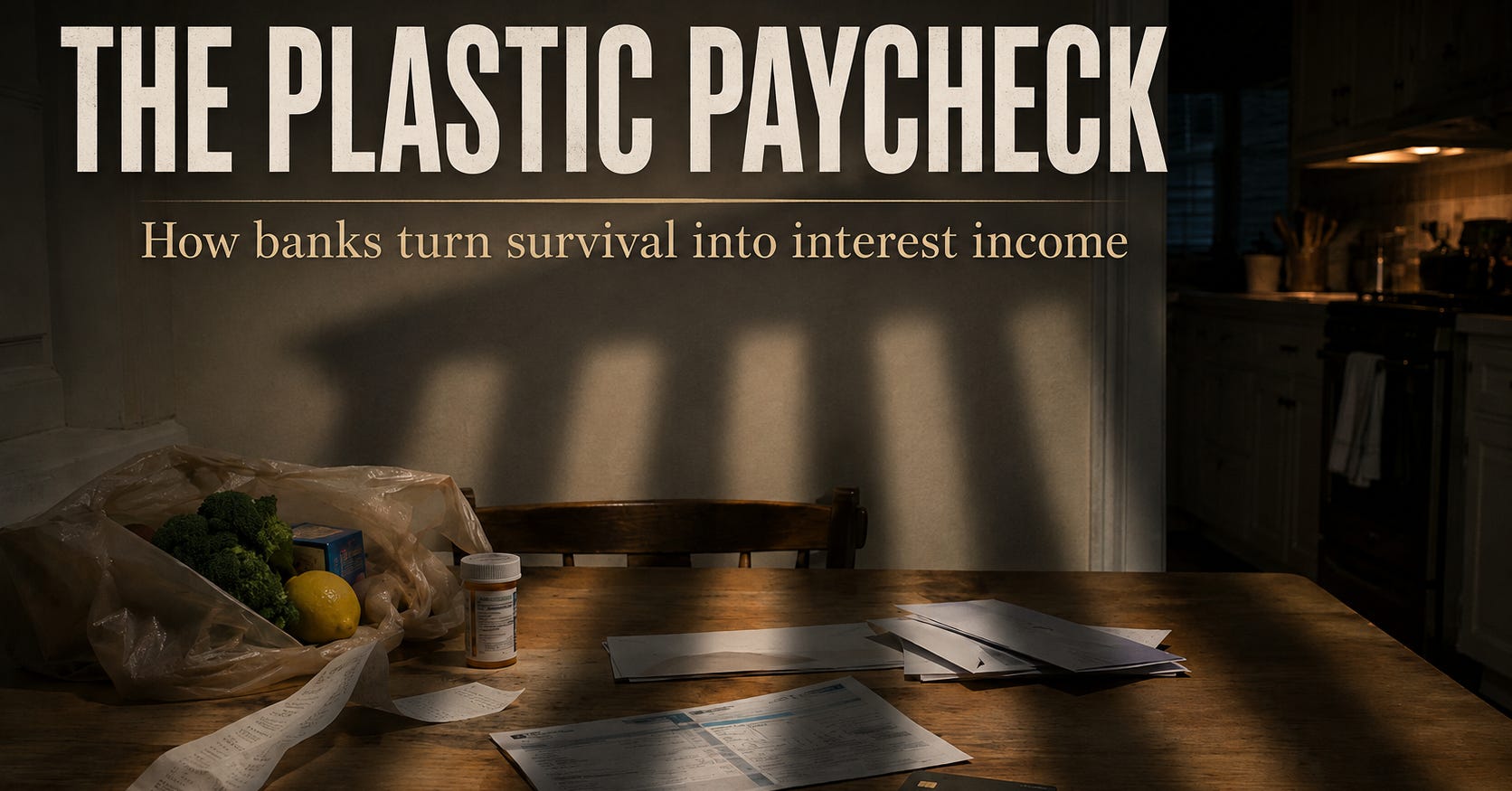

The next credit crisis in America may not begin with a Wall Street panic, a bank run, or a breaking-news banner about markets in free fall. It may begin much more quietly, with a parent standing in a grocery checkout line, knowing the debit card will not cover the cart. So the credit card comes out.

The card is not coming out for a vacation, a luxury, or some reckless shopping spree that cable news can turn into a lecture about personal responsibility. It is coming out for groceries, gas, medicine, a utility bill, a school expense, or a car repair that cannot wait because the car is how the family gets to work.

Then the bill comes. The groceries are gone. The gas tank is empty again. The medicine has been taken. The utility company has moved on to the next month. But the balance remains, and the interest starts doing what interest does. It turns one hard week into a longer sentence.

That is the credit card crisis building in this country. It is not just a debt story. It is the affordability crisis with interest attached.

Credit cards have become the place where America hides the gap between what families earn and what survival costs. When rent rises, food costs more, insurance jumps, wages do not stretch, and one emergency hits a household with no savings left, the plastic becomes the bridge. But it is a bridge with a toll booth owned by the banks.

Washington loves to talk about financial responsibility when families fall behind. Politicians and pundits can always find a way to blame the person holding the bill. They ask why people borrowed, why they carried a balance, why they did not plan better, and why they did not save more.

That moral lecture changes fast when the losses start moving up the food chain. A family missing a payment is treated as a moral failure. A bank facing losses is treated as a national emergency.

That is the real story here. Millions of Americans are being told to survive an affordability crisis with private debt, while the institutions profiting from that desperation wait for Washington to protect the system if the pain ever reaches them.

Support independent media that follows the power.

The Coffman Chronicle is built to track who holds power, who abuses it, who profits from it, and who pays the price.

Paid supporters get full Tony Michaels Podcast episodes, deeper transcript analysis, paid columns, archives, and the reporting framework behind the show.

If you believe independent media has to survive outside billionaire platforms, corporate media, and party-approved gatekeepers, become a paid supporter today.

This Is Not Just Debt. This Is Delayed Pain.

Calling this a credit card problem makes it sound smaller than it is.

A credit card balance looks like a private number on a private statement. It has a due date, a minimum payment, an interest rate, and a warning about what happens if the payment is late. On paper, it belongs to one household. In real life, that balance may carry an entire economy’s failure to make basic survival affordable.

This is what happens when the paycheck no longer matches the month. The rent does not care that groceries went up. The electric bill does not care that the car needed tires. The pharmacy does not care that the insurance premium jumped. Real life does not arrive in neat little categories. It arrives all at once, and the household has to decide which bill gets paid first.

That is where the credit card becomes dangerous. It does not feel like a crisis in the moment. It feels like a solution. It buys time. It keeps the lights on. It gets the car back on the road. It puts food in the refrigerator. It keeps a family from falling through the floor today. Tomorrow still comes.

Millions of Americans are not using credit cards because they are confused about money. Many are using them because they understand money very well. They know the landlord will not wait, the kid still needs lunch, the job still requires transportation, and the body still needs medicine. They know being broke does not stop life from charging full price.

The moral lecture is so dishonest. It treats debt like a character flaw while ignoring the pressure that created it. Some people overspend. Some people make bad choices. But a national pattern of rising credit stress cannot be explained by pretending millions of households woke up one morning and forgot how math works. This is not just debt. It is delayed pain.

It is the car repair pushed into next month, the grocery bill turned into a balance, the medical copay turned into interest, and the utility bill paid with borrowed money so the family can avoid a shutoff notice.

Credit cards have become the emergency room of the American economy. They treat the immediate bleeding, but they do not cure the injury. Then the interest comes due, and the same household that was already short is asked to pay extra for having been short in the first place.

That is not personal responsibility. That is a trap built on survival.

The Numbers Are Flashing Yellow

The numbers do not say the whole financial system is collapsing tomorrow. Panic is not the same thing as analysis, but the data is flashing yellow.

The New York Fed reported that total household debt reached roughly $18.8 trillion in the first quarter of 2026, with credit card balances around $1.25 trillion. The Federal Reserve’s consumer credit data showed that revolving credit climbed again, while credit card interest rates remained around 21%. TransUnion reported that more than 175 million consumers carried a bank card balance, with average credit card debt per borrower of around $6,500. Those are not abstract numbers but instead pressure points.

A household with savings can treat a credit card like a convenience. One without savings may have to treat it like an emergency fund with a punishing interest rate attached. It may be the same piece of plastic, but it does not function the same way depending on who is holding it.

That divide is the warning. America does not have a one-credit-card economy. It has two.

One economy uses credit cards as a tool, the other as a lifeline. One pays the balance and gets rewarded with points, perks, miles, and cash back. The other carries the balance and gets charged for needing time. One side gets perks. The other side pays the interest that helps fund the perks.

A crisis does not have to announce itself with a stock-market crash before it becomes real for working people. For a bank, a late payment is a line in a report. For a family, it can be the start of a chain reaction: a late fee, a higher balance, a lower credit score, a more expensive car loan, an apartment denied, or fewer choices the next time life breaks something.

The danger is not only how much people owe, but what they had to borrow for, how much it costs to carry that debt, and how little protection they have if the next bill comes before the next paycheck.

The quarterly line may wiggle, but household pressure is rising.

The Interest Is the Trap

Debt sounds simple when politicians and pundits talk about it. You borrowed the money, so you owe the money. End of story.

However, credit card debt does not work like a simple handshake loan between neighbors. It is a machine. Once a household carries a balance, the machine starts taking a monthly cut. If the family cannot pay the full amount, interest gets added. If another emergency hits before the balance is gone, the machine gets fed again.

That is how a grocery bill becomes a long-term payment plan, how a car repair follows a family for months, and how one medical bill turns into three problems: the original cost, the interest on the cost, and the credit damage if the household cannot keep up.

The minimum payment can make a household feel like it is staying afloat while the debt underneath keeps pulling. The account stays open, and the statement says the family is current, but being current is not the same thing as being free.

A minimum payment can keep the collector away without giving the family a real path out. It can turn a crisis into a subscription. Every month, the household pays enough to avoid immediate punishment, but not enough to escape the balance. The bank gets paid for the delay. The family gets another month of pressure.

That is the cruelty of high-interest survival debt. The original purchase may have been necessary. The interest is the penalty for not having enough cash at the right moment.

The system rewards the customer who does not need the credit and punishes the customer who does. The bank does not just collect on what people bought. It collects on the fact that they needed time.

Who Benefits, Who Pays

Every debt trap has two sides. On one side is the household trying to make the month work. On the other side is the financial system built to profit when the month does not work.

Banks benefit when people carry balances. Card issuers profit when interest keeps flowing. Payment networks reap rewards when transactions keep moving. Debt collectors rejoice when accounts go bad. An entire financial ecosystem can profit from the fact that ordinary families do not have enough cash at the exact moment life demands payment.

That does not mean every credit card product is evil or every person in the industry is sitting around plotting against working families like a cartoon villain. It is structural. The system is designed so that the household with the least room to breathe often becomes the most profitable customer.

The family that pays the balance in full can collect points, miles, cash back, fraud protection, and convenience, while the family that cannot pay in full becomes the revenue stream. Their interest helps fund the rewards economy enjoyed by people who never needed to carry the balance in the first place. One person’s perks are often subsidized by another person’s pressure.

The costs do not stay on the statement, either. A missed payment can damage a credit score, making the next car loan more expensive. It can make housing harder to secure. It can reduce access to affordable credit and turn a temporary emergency into a more expensive life.

That is how private debt becomes public damage. A bad month can become a bad credit score, and a bad credit score can become a more expensive life. That is the real cost hiding behind the minimum payment.

Congress Is Not a Bystander

Congress is not some helpless spectator standing outside the credit card market with its hands in its pockets. It has power over commerce, banking rules, consumer protection, bankruptcy law, hearings, investigations, and the rules that decide whether financial power serves the public or feeds on it.

When Congress does nothing, that is not neutrality. That is permission.

It is permission for the market to decide how much interest is too much. It is permission for lobbyists to shape the rules before working families even know the rules are being written. It is permission for banks to treat household desperation as a revenue model while elected officials pretend this is all a matter of individual budgeting.

That is the constitutional failure hiding inside the credit card crisis.

Article I does not exist so Congress can perform outrage after the damage is done. It exists so the people’s branch can debate national problems in public before private power writes the answer for everyone else.

The problem is not that every credit card regulation would be simple. It would not be. Interest caps, fee limits, credit access, underwriting standards, bankruptcy rules, consumer protections, and payday-lending risks all require serious debate. A badly designed rule can create new problems. That is exactly why Congress should be debating it in the open instead of letting bank lobbyists, campaign donors, regulators, and private executives shape the outcome behind closed doors.

A household cannot negotiate the structure of the credit card market. A parent buying groceries on borrowed money cannot personally redesign interest-rate policy. A worker trying to keep the car running cannot walk into a bank boardroom and demand a fairer system.

That is why public power exists. Government is not supposed to replace personal responsibility. It is meant to ensure that personal responsibility is not used as an excuse for private exploitation.

Congress knows how to move quickly when banks are nervous. It knows how to hold emergency meetings, write rescue packages, calm investors, and protect financial plumbing when the people at the top say the system is at risk. The question is why that urgency rarely shows up when the emergency is already happening at the kitchen table.

When Congress leaves families alone with the banks, the banks write the rules at the kitchen table.

The Watchdog Problem

A country staring at rising credit card stress should want a strong consumer watchdog. That was supposed to be the role of the Consumer Financial Protection Bureau. It was created after the financial crisis because the country learned a painful lesson: consumer finance cannot be left to police itself.

A strong CFPB can investigate abusive practices, expose junk fees, scrutinize credit card terms, examine debt collection practices, and force powerful financial institutions to answer questions they would rather bury in fine print. That only works if the watchdog is allowed to watch.

At the exact moment Americans need more protection from high-interest debt, Washington is moving in the opposite direction. The bureau has been treated less like a public shield and more like an ideological target. Its funding, staffing, enforcement power, and independence have all been put in the political grinder.

Then comes the revolving door. In June 2026, Trump nominated Brian Johnson, a former CFPB official and recent Capital One executive, to lead the bureau. Capital One is one of the largest credit card issuers in the country. When someone connected to the industry being watched is chosen to run the watchdog, the public has every right to ask who is being protected.

Concentrated power protects itself. It does not always kick down the front door. Sometimes it walks through the personnel office. Sometimes it turns the referee into a former player. Sometimes it tells the public that the watchdog is too aggressive, too independent, too burdensome, or too powerful for its own good. The real question is too powerful for whom?

For working families, the CFPB is not too powerful. It is one of the few institutions that are even supposed to be looking in their direction.

The credit card market does not need less scrutiny right now. It needs more. Instead, the watchdog is being weakened while the wolves are still in the yard. When the referee comes from the team that profits from the game, the public has a right to ask who the rules are really for.

When Main Street Breaks Before Wall Street Notices

The credit card crisis will not necessarily look like one big explosion. That is part of what makes it easy for Washington to ignore.

It may look like a family making one late payment, then falling further behind as interest accrues faster than the balance comes down. It may look like a credit limit getting cut right when a household needs it most. It may look like a card being closed after years of payments because the bank’s risk model changed. It may look like collection calls, lawsuit notices, and families deciding which bill to ignore this month so another can be paid.

It may also look like people spending less at the local diner, hardware store, barbershop, mechanic, grocery store, and other small businesses that depend on working people having a little room to breathe.

That is how a private debt problem becomes a community problem. When more income goes to interest, less income stays in town. Less money goes to local shops. Less money goes to repairs. Less money goes to school clothes, birthday presents, weekend meals, dental appointments, and the ordinary spending that keeps a community alive.

The crisis does not have to crash Wall Street to wreck Main Street. Washington often waits for a market signal. Families do not have that luxury. Their signal is the overdraft notice, the declined card, the collector’s phone call, and the bill they hide under a stack of other bills because opening it will not create money that is not there.

When the same story keeps repeating, it is not just a series of private failures. It is a public warning, and if enough floors drop at once, the people at the top will suddenly notice the building is shaking.

When People Default, Wall Street Calls It a Systemic Risk

If enough people cannot pay their credit card debt, the pain does not disappear. It moves.

For the household, the chain is brutal. A missed payment becomes a late fee. The late fee increases the balance. The credit score takes a hit. The account may get closed. The debt may be charged off by the bank. Then the collection letters begin. Then the phone calls. Then, in some cases, the lawsuit.

If a collector wins in court, a debt that began with groceries, gas, medicine, or a car repair can turn into a judgment that follows a person into wages, bank accounts, housing applications, and future credit. That is what default looks like for ordinary people, like punishment.

For banks, default has a different name. It becomes a loss, a charge-off. It becomes a risk model, a quarterly earnings problem, a lending-standard problem, a credit-tightening problem. If enough losses pile up in enough places, it becomes something powerful people start calling systemic.

That is the double standard at the heart of this entire story. A family missing a payment is treated as a moral failure. A bank facing losses is treated as a national emergency.

That does not mean Washington would immediately write a check to every credit card company. That is not how the rescue would likely be sold. The language would be cleaner. They would talk about preserving credit access, protecting the banking system, stabilizing consumer lending, liquidity, confidence, and financial plumbing, and mitigating contagion. They would say they are not saving banks. They are saving the economy.

Working families know how this story usually goes. When the crisis is trapped at the kitchen table, it is called personal responsibility. When the crisis climbs high enough to reach the balance sheets of powerful institutions, it becomes everybody’s problem.

People are told there is no money for relief, no political room for stronger protections, no easy way to regulate interest rates, no simple answer on junk fees, and no practical path to bankruptcy reform. Yet when financial institutions are in danger, Washington suddenly remembers how to move. The calendars clear. The emergency meetings happen. The experts are summoned. The rescue language appears. The same lawmakers who could not find urgency for families somehow find urgency for markets.

This is why the credit card crisis must be discussed before losses peak. If Congress waits until the banks are nervous, the first draft of the solution will be written for banks.

The people absorb the crisis first. The institutions ask for protection later. Unless Congress acts before that moment, the rescue will be framed around the health of the financial system rather than the people whose pain fed it in the first place.

Public power should not wake up only when private power gets scared.

What Congress Should Be Debating

This is why Congress should be forced out of hiding. Congress should be asking why credit card interest rates remain so high when the public is already stretched thin. It should be asking how much profit comes from revolving balances, penalty rates, late fees, and people who cannot afford to pay in full. It should be asking whether minimum-payment rules are designed to help people escape debt or simply keep them current enough to remain profitable. Those are not radical questions. They are oversight questions.

Congress should be asking whether late fees and junk fees are being used as another extraction point from households that are already cornered. It should be asking whether penalty interest rates are reasonable or function as punishment piled on top of hardship. It should be asking how many Americans are carrying balances for groceries, gas, medicine, utilities, and emergency repairs.

Congress should also be debating bankruptcy law, interest caps, credit access, payday-lending risks, and the future of the CFPB. None of those debates is simple. That is the point. A serious government does not run from tradeoffs. It drags them into the light.

This is also where both parties should be put on the record. Republicans should not be allowed to talk about working-class pain while weakening the agencies that protect working-class people from financial abuse. Democrats should not be allowed to treat credit card anger as a campaign message while failing to force the issue through hearings, legislation, amendments, and public pressure.

The people do not need another round of financial theater. They need lawmakers willing to use power. That is the Article I demand. Hold the hearings. Subpoena the executives if necessary. Put the interest rates on a screen. Record the fee revenue. Put the lobbyists under oath. Ask who pays, who profits, who gets protected, and who gets blamed. Then write law.

The country does not need another speech about financial responsibility from people who refuse to regulate financial power. It needs a Congress willing to decide whether credit is meant to serve the economy or the economy is meant to serve the credit industry.

The Plastic Paycheck Is Breaking

The family at the grocery checkout did not swipe because they were living large. They swiped because the cart had food in it, the paycheck was not there yet, and the kids still needed to eat. They swiped because the car had to get fixed, because the prescription could not wait. They swiped because the electric bill was due, the rent was higher, the insurance premium jumped, and real life does not pause while Washington argues over whether working people deserve protection.

That is what this crisis is really about. It is not about whether every borrower made every perfect choice. Nobody lives a perfect life inside a broken economy. The question is whether America is going to keep pretending that millions of households falling into the same trap is just millions of separate moral failures.

Credit cards have become a private patch on a public failure. They are being used to cover the distance between wages and survival, between the bill and the paycheck, between the emergency and the savings account that never had a chance to exist. Every time that patch is used, banks get another chance to turn household pressure into interest income.

That is not a stable economy. That is an economy outsourcing its pain to families and monetizing the delay.

Congress can keep pretending this is none of its business. It can keep letting banks write the rules at the kitchen table. It can wait until defaults rise, credit tightens, and the financial system starts using emergency language. It can wait until the same people who ignored household pain suddenly demand action to protect markets, or it can act like the people’s branch before the people are crushed.

The credit card crisis is not coming because Americans forgot how to budget. It is coming because survival keeps costing more than millions of households can carry, and the system has decided to charge them interest for needing time.

A country that can rescue banks can protect families. A Congress that can move for markets can move for people. A republic that belongs to the people should not wait until private power gets scared before public power wakes up.

America does not need to shame people for drowning while banks sell them buckets of water. It needs a Congress willing to ask who built the flood, who profits from the rescue, and why working families keep paying interest on a crisis they did not create.

Support Independent Media

If this article helped you see the credit card crisis as more than a personal finance problem, share it with someone who is tired of working people being blamed for a system built to profit from their pressure.

And if you can afford to become a paid subscriber, your support helps keep Coffman Chronicle independent, people-powered, and focused on the fights Congress would rather avoid.

Sources:

“Trump Names Former CFPB Official Brian Johnson to Be Agency’s Next Permanent Director.” AP News, June 10, 2026.

“Consumer Credit—G.19: April 2026.” Federal Reserve, June 5, 2026.

“Commercial Bank Interest Rate on Credit Card Plans, All Accounts [TERMCBCCALLNS].” FRED, Federal Reserve Bank of St. Louis.

“Building the CFPB.” Consumer Financial Protection Bureau, August 8, 2023.

“The Consumer Credit Card Market.” Consumer Financial Protection Bureau, December 30, 2025.

“The Consumer Credit Card Market Report to Congress.” Consumer Financial Protection Bureau, 2025.

“A Borrower’s Guide to an FDIC Insured Bank Failure.” FDIC, June 18, 2024.

“Household Debt Balances Rise Slightly as Delinquency Transition Rates Hold Steady.” Federal Reserve Bank of New York, May 12, 2026.

“Quarterly Report on Household Debt and Credit: 2026.” Federal Reserve Bank of New York, May 2026.

“Uniform Retail Credit Classification and Account Management Policy.” Federal Reserve Bank of New York, March 2, 1999.

“Consumer Credit Card Market Report of the Consumer Financial Protection Bureau, 2025.” Federal Register, January 7, 2026.

“Debt Collection FAQs.” FTC Consumer Advice.

“U.S. Consumer Credit Market Increasingly Splitting Along a K-Shaped Path, TransUnion Research Finds.” TransUnion Newsroom, April 30, 2026.

“Article I, Section 8, Clause 3: Commerce Clause.” Constitution Annotated.

“Troubled Asset Relief Program (TARP).” U.S. Department of the Treasury.

Along with the credit card debt comes this regime throwing all on ACA to the sharks. Yep this regime wants people who can’t pay their medical bills to take loans from… health insurance companies.

Can’t Pay Medical Bills? Trump Officials Suggest Getting a Loan

https://www.nytimes.com/2026/06/11/business/aca-health-care-costs-medical-debt.html

Well Said 🔝🦉